Aug

13

2024

A retirement gap analysis helps individuals identify a potential shortfall between how much they have saved and what they will need in retirement.

Tallying all accounts, projecting ahead, then comparing that amount to how much a fully funded retirement costs, given your unique circumstances, can help people bridge the financial gap between the present and retirement. It’s a great way to visualize how you are tracking towards your retirement goals.

A retirement analysis is typically a report a financial advisor creates for individuals who want to know if they are on track for retirement. The analysis can also be done using online tools. Saving for retirement is an important process for those who are looking forward to a secure future with a steady stream of income.

Knowing the difference between what you have saved versus what you will need in order to retire on time is valuable information to determine if you are on track for retirement. If necessary, you can then take extra steps to boost your savings rate once you have a retirement gap analysis and risk assessment performed. This might include such actions as changing your investing strategy or considering annuities, for instance.

A retirement gap analysis considers a range of retirement assets. Your 401(k) through your employer, any individual retirement accounts you might own, annuities, individual taxable brokerage accounts, and even Social Security are common assets to tally in a retirement gap analysis. The sum of those assets is then compared to what you will need in the future, so that you can retire with confidence.

Conducting a retirement analysis can be done using online tools or by meeting with a financial advisor. It’s all about knowing when you can retire. Often, individuals will take action to improve their financial habits and retirement savings when they see what they must do.

For example, a retirement gap on a chart can be a powerful visual to inspire people to save more. Performing a retirement analysis requires careful input of all assets and some assumptions about future rates of return, as well as a person’s spending habits and goals in order to determine how long their savings and other assets may last.

Assets and liabilities are analyzed, and future cash flow is projected. Conducting a retirement analysis also includes estimating how long somebody might live. Longevity risk is a key consideration, and Social Security and annuities can help reduce the risk of running out of money. There are many facets to performing a retirement gap analysis. Seeking out the help of an experienced fiduciary advisor may be helpful so that you are confident in your retirement plan.

A critical factor of a retirement analysis is the communication aspect. This is where a financial planner could potentially show their skills.

Simply looking over investment accounts and seeing numbers on a spreadsheet might not cause people to change course on their journey to retirement. Communicating a retirement gap in the right context can help drive home the message that saving more today will lead to a better tomorrow.

A high-level retirement gap analysis should be mixed in with detailed cash flow planning.

Your 401(k) plan is a major account that is assessed during a retirement analysis. An employer-sponsored retirement account is a large part of many workers’ overall retirement plan. A 401(k) gap can be found by analyzing the value of a participant’s pre-tax and Roth accounts versus what they will need to retire.

A 401(k) account often features an employer matching contribution, which is almost like free money so long as you meet the plan’s matching contribution requirements. Many plans will match, say, 50% of the employee’s contribution up to 6%. For a $100,000 salary, that means $3,000 per year of employer contributions, in addition to $6,000 from the employee. That’s $9,000 per year.

A 401(k) account, among other retirement plans offered through work, is typically a major piece of someone’s retirement asset pie. The process to increase contributions to it is generally easy to do. Moreover, the auto-enrollment and auto-escalation features are tools that can help more people save more for retirement so that their 401(k) gap shrinks over time. A 401(k) analysis can be helpful for workers young and old.

Let’s run through a retirement gap analysis example to better show the steps involved.

| Retirement Gap Analysis, Step-by-Step | Rationale |

|---|---|

| Retirement Income Assessment: Summing all retirement savings accounts to find a portfolio value. | Identifies any potential shortfall between required monthly income and total projected income between Social Security, retirement plans, and other accounts. |

| Review liabilities and future spending habits. | No retirement gap analysis is complete without a thorough assessment of what you owe and current and future spending. |

| Analyze changes to an individual’s retirement date. | Can make arriving at retirement easier if more time is allowed to increase saving. |

| Strategize about Social Security options. | Delaying benefits until age 70 will increase total payout; might reduce longevity risk. |

| Outlining steps to take to shore up retirement income. | Increasing a 401(k) contribution rate can help narrow the retirement gap. Reducing spending and increasing your savings rate are other actions. |

Knowing if your 401(k) is enough is important, but so too is a broader look at your assets and liabilities along with what income to expect in retirement. No retirement gap analysis is complete without it.

Calculating retirement income can be done using various online calculators, but you might want to sit down with a financial planner to map out what income you, personally, will need in retirement. Variables like your spending habits, inflation, discounted cash flow rates, and possible risks all must be considered.

You can also leverage the Social Security Administration’s Retirement Estimator calculator to find out what you should expect to receive when you decide to retire. While the output is just an estimate, it can go a long way toward bridging your retirement gap if you have a gauge of what income you will have in retirement.

Another way to calculate retirement income is to sum up your retirement assets, assume a contribution rate between now and retirement along with a rate of return, then take that asset base as an amount from which to draw income during retirement.

Many planners use the “4% rule”, which states that a retiree can withdraw up to 4% of their retirement account value each year without a high risk of running out of money. This is just a rule of thumb, however, and it might not work as well today as it did decades ago.

Identifying where you are on your retirement journey is an important part of financial planning. Doing a retirement gap analysis is an essential part of that process. As time passes, our lives and lifestyles, our goals, and often our physical health can change. All these factors can impact how much we’ll need to spend in the future.

By conducting a retirement gap analysis to identify any shortfalls in savings, it’s possible to make adjustments, and course-correct to get savings goals on track.

Prepare for your retirement with an individual retirement account (IRA). It’s easy to get started when you open a traditional or Roth IRA with SoFi. Whether you prefer a hands-on self-directed IRA through SoFi Securities or an automated robo IRA with SoFi Wealth, you can build a portfolio to help support your long-term goals while gaining access to tax-advantaged savings strategies.

Easily manage your retirement savings with a SoFi IRA.

A retirement gap is a difference in the amount you have saved for retirement versus how much you will need. A retirement gap analysis can be performed to help identify how much more you will need to save for retirement. Once you know the amount, you can then take steps to boost your savings and investment accounts so that you can retire on time.

Many individuals have a 401(k) or another retirement plan through their employer. Check with your HR department to see if there is an account set up for you. You might also have retirement accounts established on your own through investment brokerage companies. Also consider that you can likely collect a monthly Social Security benefit in retirement. Be sure to check with the Social Security Administration.

This is a tough question, but an important one. Knowing how much you will need for retirement is crucial to developing a retirement savings strategy and living a confident retirement. You may want to meet with a financial advisor to develop a plan. You can also use online resources, tools, and calculators to help determine if your current portfolio is enough to fund your retirement.

Photo credit: iStock/MicroStockHub

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

SOIN-Q324-020

Read more

When a financial analyst rates a stock as overweight, it means that the analyst believes an overweight stock will likely outperform other stocks in its industry over the next six to 12 months. Conversely, if they describe a stock as underweight, they believe that it will perform poorly in the future.

It may be helpful to think of these terms as pointers: as if an industry specialist were saying, “You might want to overweight Stock X in your portfolio” or “maybe you should under-weight Stock Y.” These ratings are typically the result of factors in the news or pertaining to a specific company’s prospects. But the terms “overweight” and “underweight” also refer to a stock’s weighting in a relevant index or benchmark.

Key Points

• An overweight stock rating indicates that analysts expect the stock to outperform its industry peers within the next six to twelve months.

• The terms overweight and underweight also refer to a stock’s proportion in an investment portfolio, guiding investors on how much to hold.

• Different market indexes apply unique weighting systems, influencing how stocks are rated as overweight or underweight based on market capitalization or stock price.

• Investors should be cautious, as an overweight stock may not always lead to significant gains and could lead to portfolio imbalance if not managed properly.

• The context of both the market and individual portfolios is crucial when interpreting overweight ratings, emphasizing the need for careful investment decisions.

As noted, an overweight stock is one that analysts believe will outperform others in its sector or market segment in the near future. Similarly, overweight stock is a moniker that may also describe a specific security’s weighting in a portfolio, and one that analysts think investors should buy more of – so, its meaning can be contextual in certain situations.

💡 Quick Tip: How to manage potential risk factors in a self-directed investment account? Doing your research and employing strategies like dollar-cost averaging and diversification may help mitigate financial risk when trading stocks.

To understand stock ratings related to weight, it’s important to know that market indexes assign a weight to the investments they track to be sure that the index accurately reflects the performance of that market sector.

For example, the S&P 500® tracks 500 large-cap U.S. companies. The companies in the index — called the constituents — are weighted by market capitalization. A company’s market cap is calculated by multiplying the current share price by the total number of outstanding shares.

Companies in that index are weighted based on the proportion of the overall index their market cap represents. Other indexes may use a different weighting system. The Dow Jones Industrial Average, for example, tracks 30 blue chip companies and weights them based on stock price. Companies with a higher share price are given more weight than those with lower prices.

Because of these different weighting systems, it’s important to understand that an overweight to a particular stock with regards to one index may not be the same when it comes to another.

When an analyst rates Stock X as overweight, it’s generally a positive sign. First, they believe Stock X is likely to outperform its benchmark index, or even the market as a whole, depending on market conditions, so investors should consider holding more of the stock.

Bear in mind that an “overweight stock” rating doesn’t necessarily mean that stock is a juggernaut. In a down market, being overweight could simply mean the company might not lose as much ground as its peers, or it might grow less slowly than its peers.

When an analyst rates Stock Y as underweight, the analyst believes that Stock Y is likely to underperform its benchmark, and investors should consider holding less of this stock.

When an analyst gives an equal weight rating to a stock, that simply means it’s in line with the overall benchmark. Again, when considering these ratings it’s important to keep in mind the overall context of the market, and what these ratings mean to analysts.

A very simple example of an overweight stock could be when a stock, Stock X, is selling for $50, but experts and analysts think it’s undervalued and should trade for $75, it could be overweight.

Further, an overweight stock rating can be taken in two ways: First, that the stock will outperform its benchmark index and second that investors may want to take advantage of the increase in price.

When an analyst indicates their belief that a stock will appreciate, they may also state a potential time frame and price target for the stock. So, if Stock X is trading at $75 per share, and the company releases new earnings data that’s positive, an analyst might rate the stock as overweight, with a price target of $100 per share in the coming year.

One critique of this rating system is that no analyst, of course, can recommend how many shares investors should buy. It’s simply not possible for analysts to know whether Investor A’s portfolio might benefit from an additional 100 shares of Stock X, while Investor B might want to buy 1,000 shares of Stock X.

As a result, it’s incumbent on individual investor’s themselves to keep an eye on how relevant an overweight stock rating might be for their specific allocation. Buying more of Stock X could, in theory, create an imbalance and reduce a portfolio’s overall diversification. So while an overweight stock might be a good thing, an overweight portfolio usually is not.

At first glance, the terms overweight and underweight may seem more or less synonymous with “buy” and “sell” — in that case, why don’t analysts use these more straightforward terms?

In fact, the terms overweight and underweight do have a slightly different connotation than simply to buy or sell a security. Rather, the terms suggest a recommendation that a portfolio hold more or less of a particular position than an index or other benchmarks would suggest.

It may mean acquiring more, or selling some, of a particular investment. But it wouldn’t necessarily mean buying something new or selling all of a position. For example, if your portfolio has an allocation to tech stocks, and an analyst recommends overweighting one of those stocks, you may want to buy more of that company. Or you may not need more growth in your tech holdings, so you might look for an overweight stock.

Also, analysts aren’t always comfortable giving specific directions to buy or sell certain securities. The terms overweight and underweight are more like offering guidance: “Here’s what I think of Stock X or Stock Y. I’ll let the investor take it from here.”

In many cases an overweight or underweight recommendation might not be very useful for investors. For example, if an analyst recommends an overweight to a certain commodity but an investor’s portfolio doesn’t hold any commodities, this information may not have much bearing on their situation.

Overweight can refer to a portfolio that holds more of a stock or other investments than it theoretically should. For individual investors, this might mean that more of a portfolio is allocated to stock than the investor intended.

For example, say an investor has a portfolio allocation in which 70% of its allocation is held in stock and 30% is held in bonds. If the stock market goes up, the proportion of the portfolio held in stock may grow beyond the 70% mark. At that point, the portfolio may be described as overweight in stocks, and an investor may want to rebalance to bring it in line with their initial allocation plan.

It may come as no surprise that the opposite of an overweight allocation is an underweight allocation. For example, if the stock allocation in the portfolio above fell below 70%, that allocation could be described as underweight in stocks.

The term can also apply in a narrower sense. For example, a stock portfolio could hold too much stock in one company, sector, or geographical region. In each case the holding could be described as overweight.

Professional fund managers may also use overweight to describe portfolios they work with that are off track with their index, including mutual funds, exchange-traded funds, and index funds. From time to time, a fund may get out of line with its benchmark index by holding more or less of an investment that index tracks.

For example, say an index fund is built to track the S&P 500. To track the index, fund managers will usually attempt to hold every stock in the index. Additionally, they will try to match the proportion of each individual company their fund holds to the index as well. So if stock A represents 5% of the original index, the fund will also hold 5% of stock A.

Some funds have a little bit of wiggle room in terms of how far they can stray from the index. Some might be allowed to hold more or less stocks if they think the stocks will outperform or underperform. When they hold more than the index, the managers are taking an overweight position. And when they hold less than the index, the managers are taking an underweight position.

Overweight stocks are those that may be undervalued by the market. When an analyst gives a stock an overweight rating, broadly speaking it could be a good thing. If the analyst is correct, and the stock is indeed poised to perform better than its benchmark — maybe even better than the market as a whole — investors may want to buy that stock.

But the necessary caveat is that it all depends on context — the context of the market, and the context of an investor’s portfolio overall. You don’t want to buy a stock that could throw your allocation off, and make your portfolio overweight in a way that’s not ideal.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.¹

An overweight stock can be good for investors looking for a relative deal, but it may not be a good thing if the investor already owns shares of the stock.

Outperform stocks and overweight stocks are similar, and the terms are often used interchangeably. But generally, “outperform” may describe a stock that’s undervalued or expected to offer solid returns in the future, but perhaps perform not quite as well as an “overweight” stock.

On an analysts’ rating system, “buy” and “overweight” stocks are rated differently, with “buy” being a higher rating – though both ratings are positive.

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

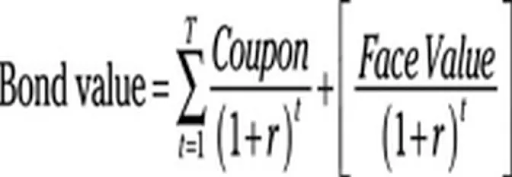

Bond valuation is a way of determining the fair value of a bond. Bond valuation involves calculating the present value of the bond’s future coupon payments, its cash flow, and the bond’s value at maturity (or par value), to determine its current fair value or price. The price of a bond is what investors are willing to pay for it on the secondary market.

When an investor buys a bond from the issuing company or institution, they typically buy it at its face value. But when an investor purchases a bond on the open market, they need to know its current value. Because a bond’s face value and interest payments are fixed, the valuation process helps investors decide what rate of return would make that bond worth the cost.

Key Points

• Bond valuation is the process of determining a bond’s fair value by calculating the present value of future coupon payments and its value at maturity.

• Investors must consider the bond’s current price, which may differ from its face value, as it reflects market conditions and the issuing company’s creditworthiness.

• The valuation involves discounting the bond’s future cash flows using a realistic discount rate, which is essential due to the time value of money.

• Changes in interest rates significantly affect bond pricing; rising rates usually decrease bond prices, while falling rates can increase them.

• Investing in bonds can diversify a portfolio, as they tend to be less risky than stocks and provide a predictable income stream through fixed payments.

First, it’s important to remember that bonds are generally long-term investments, where the par value or face value is fixed and so are the coupon payments (the bond’s rate of return over time) — but interest rates are not, and that impacts the present or fair value of a bond at any given moment.

To determine the present or fair value of a bond, the investor must calculate the current value of the bond’s future payments using a discount rate, as well as the bond’s value at maturity to make sure the bond you’re buying is worth it.

Some terms to know when calculating bond valuation:

• Coupon rate/Cash flow: The coupon rate refers to the interest payments the investor receives; usually it’s a fixed percentage of the bond’s face value and typically investors get annual or semi-annual payments. For example, a $1,000 bond with a 10-year term and a 3% annual coupon would pay the investor $30 per year for 10 years ($1,000 x 0.03 = $30 per year).

• Maturity: This is when the bond’s principal is scheduled to be repaid to the bondholder (i.e. in one year, five years, 10 years, and so on). When a bond reaches maturity, the corporation or government that issued the bond must repay the full amount of the face value (in this example, $1,000).

• Current price: The current price is different from the bond’s face value or par value, which is fixed: i.e. a $1,000 bond is a $1,000 bond. The current price is what people mean when they talk about bond valuation: What is the bond currently worth, today?

The face value is not necessarily the amount you pay to purchase the bond, since you might buy a bond at a price above or below par value. A bond that trades at a price below its face value is called a discount bond. A bond price above par value is called a premium bond.

💡 Quick Tip: Are self-directed brokerage accounts cost efficient? They can be, because they offer the convenience of being able to buy stocks online without using a traditional full-service broker (and the typical broker fees).

Bond valuation can seem like a daunting task to new investors, but it is not that onerous once you break it down into steps. This process helps investors know how to calculate bond valuation.

The bond valuation formula uses a discounting process for all future cash flows to determine the present fair value of the bond, sometimes called the theoretical fair value of the bond (since it’s calculated using certain assumptions).

The following steps explain each part of the formula and how to calculate a bond’s price.

A bond’s cash flow is determined by calculating the coupon rate multiplied by the face value. A $1,000 corporate bond with a 3.0% coupon has an annual cash flow of $30. If it’s a 10-year bond that has five years left until maturity, there would be five coupon payments remaining.

Payment 1 = $30; Payment 2 = $30; and so on.

The final payment would include the face value: $1,000 + $30 = $1,030.

This is important because the closer the bond is to maturity, the higher its value may be.

The coupon payments are based on future values and thus the bond’s cash flow must be discounted back to the present (thanks to the time value of money theory, a future dollar is worth less than a dollar in the present).

To determine a discount rate, you can check the current rates for 10-year corporate bonds. For this example, let’s go with 2.5% (or 0.025, when expressed as a decimal).

Calculate the present value of future cash flows including the principal repayment at maturity. In other words, divide the yearly coupon payment by (1 + r)t, where r equals the discount rate and t is the remaining payment number.

$30 / (1 + .025)1 = $29.26

$30 / (1 + .025)2 = 28.55

$30 / (1 + .025)3 = 27.85

$30 / (1 + .025)4 = 27.17

$1030 / (1 + .025)5 = 1,004.87

Sum all future cash flows to arrive at the present market value of the bond : $1,117.70

In this example, the price of the bond is $1,117.70, or $117.70 above par. A bond’s face or par value will often differ from its market value — and in this case its current fair value (market value) is higher. There are a number of factors that come into play, including the company’s credit rating, the time to maturity (the closer the bond is to maturity the closer the price comes to its face value), and of course changes to interest rates.

Remember that a bond’s price tends to move in the opposite direction of interest rates. If prevailing interest rates are higher than when the bond was issued, its price will generally fall. That’s because, as interest rates rise, new bonds are likely to be issued with higher coupon rates, making the new bonds more attractive. So bonds with lower coupon payments would be less attractive, and likely sell for a lower price. So, higher rates generally mean lower prices for existing bonds.

The same logic applies when interest rates are lower; the price of existing bonds tends to increase, because their higher coupons are now more attractive and investors may be willing to pay a premium for bonds with those higher interest payments.

Investing in bonds can help diversify a stock portfolio since stocks and bonds trade differently. In general, bonds are seen as less risky than equities since they often provide a predictable stream of income. Investors can consider bonds as an investment, and those with a lower risk tolerance might be better served with a portfolio weighted highly in bonds.

Performing proper bond valuation can be part of a solid research and due diligence process when attempting to find securities for your portfolio. Moreover, different bonds have different risk and return profiles. Some bonds — such as junk bonds and fixed-income securities offered in emerging markets — feature higher potential rates of return with greater risk. “Junk” is a term used to describe high-yield bonds. You can take on higher risk with long-duration bonds and convertible bonds. Some of the safest bonds are short-term Treasury securities.

You can also purchase bond exchange-traded funds (ETFs) and bond mutual funds that own a diversified basket of fixed-income securities.

Bond valuation is the process of determining the fair value of a bond after it’s been issued. In order to price a bond, you must calculate the present value of a bond’s future interest payments using a reasonable discount rate. By adding the discounted coupon payments, and the bond’s face value, you can arrive at the theoretical fair value of the bond.

A bond can be priced at a discount to its par value or at a premium depending on market conditions and how traders view the issuing company’s prospects. Owning bonds can help diversify your portfolio. Many investors also find bonds appealing because of their steady payments (one reason that bonds are considered fixed-income assets).

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.¹

Photo credit: iStock/Tempura

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by emailing customer service at [email protected]. Please read the prospectus carefully prior to investing.

Fund Fees

If you invest in Exchange Traded Funds (ETFs) through SoFi Invest (either by buying them yourself or via investing in SoFi Invest’s automated investments, formerly SoFi Wealth), these funds will have their own management fees. These fees are not paid directly by you, but rather by the fund itself. these fees do reduce the fund’s returns. Check out each fund’s prospectus for details. SoFi Invest does not receive sales commissions, 12b-1 fees, or other fees from ETFs for investing such funds on behalf of advisory clients, though if SoFi Invest creates its own funds, it could earn management fees there.

SoFi Invest may waive all, or part of any of these fees, permanently or for a period of time, at its sole discretion for any reason. Fees are subject to change at any time. The current fee schedule will always be available in your Account Documents section of SoFi Invest.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Maintenance margin, as it relates to margin accounts and trading, refers to the necessary amount of funds an investor needs to maintain in their brokerage account in order to utilize margin. Margin accounts work differently than other trading accounts. Instead of allowing the trader to do regular trades, the margin account allows leveraged trades.

This means that the trader can buy securities including stocks, bonds, or options for more than the amount that they have in their account, paying only a deposit on the trade. They borrow the rest of the cash needed for the investment from the broker.

Key Points

• Maintenance margin represents the minimum balance required in a trader’s margin account to avoid a margin call and continue leveraged trading.

• The Financial Industry Regulatory Authority mandates a minimum maintenance margin of 25%, but individual brokerage firms often set higher requirements for added security.

• Margin trading carries significant risks, as traders can incur losses exceeding their account balance, leading to margin debt owed to brokers.

• If a trader’s account balance falls below the maintenance margin, the broker can issue a margin call, requiring additional funds or asset liquidation within a specified timeframe.

• Understanding the distinction between maintenance margin and initial margin is crucial, as the initial margin is the upfront deposit required to open a margin account.

In margin trading, the maintenance margin is the minimum amount of funds that a trader must hold in their portfolio to avoid being issued a margin call, for as long as they are actively involved in a trade. If a trade they enter decreases in value, the trader may owe money, which is taken from their account.

Minimum margin requirements for leveraged accounts are regulated by the government. Currently the Financial Industry Regulatory Authority (FINRA) sets the maintenance margin at 25% of the total value of securities that a trader holds in their margin account.

Specific brokerage firms also maintain their own requirements. It is common for brokerage requirements to be higher than the government required amount to provide the firm with greater financial security.

Margin maintenance requirements shift based on various factors, including market liquidity and volatility. And different stocks have differing maintenance requirements: if they are more likely to be volatile, the requirements may be higher.

Maintenance margin doesn’t mitigate risk for traders. Margin investing is risky because traders can lose more money than they have in their account, creating a debt with the broker, called margin debt.

When a trader opens a margin account, they must sign an agreement and deposit a certain amount into the account before they can start trading. To pay off any debt from assets that have lost value, the trader will need to deposit additional funds, deposit securities, or sell off holdings.

Therefore, margin trading isn’t recommended for beginner traders, and it’s important for traders to understand the risks and how it works before trying it out.

💡 Quick Tip: When you’re actively investing in stocks, it’s important to ask what types of fees you might have to pay. For example, brokers may charge a flat fee for trading stocks, or require some commission for every trade. Taking the time to manage investment costs can be beneficial over the long term.

*For full margin details, see terms.

Let’s look at an example of how maintenance margin requirements work.

Let’s say a trader wants to purchase 100 shares of Company XYZ at $40 per share. They don’t have sufficient funds to purchase the entire number of shares. The trader can use a margin account which allows them to purchase the entire amount of shares but only deposit a percentage of the total price into the trade and also pay a financing fee. This deposit amount is known as the initial margin requirement.

In this example, the initial maintenance margin requirement is 40% of the purchase price of the trade. For the trader to purchase the full 100 shares, they need to maintain a balance of 40% of the trade purchase amount in their margin account.

If the amount in their account dips below the minimum requirement, their broker will issue a margin call notification. Generally, the trader will have between 2-5 days to either add more funds to their account or sell some of the assets they are invested in to move enough cash funds back into their account.

If the trader doesn’t sell holdings or add funds to their account to meet the margin maintenance requirement, the broker may sell the trader’s securities without notifying them, and they have the right to decide which ones they sell. They are also allowed to charge the trader commissions and even sue the trader for losses.

A margin call can also be sent out if the brokerage firm changes their requirements, which they can do at any time.

Each brokerage firm has their own maintenance margin requirements. The formula to calculate the maintenance margin is:

Account value = (Margin Loan) / (1 – Maintenance Margin %)

This can be used to determine the stock price that will trigger a margin call.

For example, a trader opens a margin account and deposits $20,000 into it, then borrows $10,000 from the broker in a margin loan in order to purchase 200 shares of stock at a price of $100 each. The broker’s maintenance margin is 30%. Here is what the calculation would be to figure out what account balance would trigger the margin call:

($10,000 Margin Loan) / (1 – 0.30 Maintenance Margin %) = $14,285.71

That means that if the trader’s account dips below $14,285.71, or if the price of the stock falls below $71.43 ($14,285.71 / 200 shares) then the broker will issue a margin call.

Recommended: What Is Margin Interest and How to Calculate It

When traders open a margin account, there is an initial margin amount they are required to deposit before they can start trading. This is set by FINRA, and brokers may also have their own additional requirements. The initial margin required by FINRA is currently $2,000 in cash or securities.

After a trader starts buying on margin, they must meet the maintenance margin on their account — at least 25% of the market value of the securities in their account.

A maintenance margin is a monetary buffer for traders with margin accounts. The maintenance margin is a minimum balance required to execute leveraged trades. If a trader’s margin account dips below the minimum set by FINRA and the broker, the broker will issue a warning, or margin call, so that the trader can add cash to their account or sell holdings to cover the gap.

Maintenance margins do not mitigate risks for traders, and if an investor is utilizing margin as a part of their investment strategy, they should know what they’re getting into. Margin accounts have their pros and cons, but it’s important to keep the risks in mind.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.¹

Generally, if a trader or investor’s account goes below the maintenance margin, their brokerage will send them a margin call, or otherwise warn them that they need to deposit funds or sell holdings.

Current maintenance margin refers to the literal current maintenance margin set by financial regulators or by a specific brokerage. For example, it may be 25% of the value of an investor’s total holdings.

Minimum margin refers to the minimum amount of collateral needed in a margin account to execute leveraged trades, while maintenance margin is the total capital that needs to remain in the account as the investor continues to utilize a margin account.

FINRA currently sets the maintenance margin, which is 25%. But specific brokerage firms can set their own beyond that, and often, at a higher threshold.

Maintenance margin requirements can be determined by a number of factors beyond regulatory minimums, such as market conditions and volatility, and the specific types of securities an investor is trading.

Twenty-five percent maintenance margin means that an investor must hold 25% of the total value of their holdings in their account. It is the minimum amount of equity that must be maintained in their margin account.

Photo credit: iStock/StockRocket

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SOIN1023010

See what SoFi can do for you and your finances.

Select a product below and get your rate in just minutes.