The power hour is a period of active trading, high volume, and volatility that tends to occur when the market opens and again when it closes. Many short-term traders find the power hour appealing because of the trading opportunities it presents.

Power hour trading generally isn’t as compelling to buy-and-hold and longer-term investors, as these short-term trades come with much higher risk exposure, despite the opportunity for gains.

Key Points

• The “power hour” refers to periods of high trading activity, volume, and volatility typically at the market’s open and close.

• While appealing to short-term traders, power hour trading carries more risk for longer-term investors.

• The first hour of trading is active due to reactions to overnight news, while the last hour sees increased activity as traders look to close positions or capitalize on heightened selling.

• Triggers for intense power hour trading include earnings reports, news about “daily gainers,” major economic news, and quarterly triple witching hour events.

• Due to increased volatility and risk, it is advisable for investors unfamiliar with choppy markets to avoid power hour trading.

What Is the Stock Market Power Hour?

During the trading day, the power hour is when traders have a concentrated time to leverage specific market opportunities. That goes for anyone trading common market securities like stocks, index funds, commodities, currencies, and derivatives, especially options trading and futures.

The power hour period typically occurs when the market opens at 9:30am ET and lasts until approximately 10:30am. Some traders identify a second power hour at the end of the day: roughly 3:30pm to 4:30pm, when the market closes.

The heightened activity during these periods comes from a confluence of factors.

• Traders digest recent news and upcoming events.

• They place new trades and look for opportunities.

The term power hour is subjective, but most market observers land on two specific times in defining the term:

• The first trading hour of the market day. This is when news flows in overnight from across the world that can impact portfolio positions that investors may want to leverage, when investing online or using a brokerage.

• The last hour of the trading day. This is when sellers may be anxious to close a position for the day, and buyers trading stocks may be in a position to pounce and buy low when selling activity is high.

One commonality between the first hour of a stock market trading session and the last hour is that trading volatility tends to be higher than it is during the middle of a normal trading day. That’s primarily because traders are looking to buy or sell when demand for trading is robust, and that usually happens at or near the market opening or the market close.

Each power hour brings something different to the table, when it comes to potential investing opportunities.

The first hour of any trading session tends to be the most active, as traders react to overnight news and data numbers and stake out advantageous positions.

For example, an investor may have watched financial or business news the previous night, and is now reacting to a story, interview, or prediction.

Some traders refer to this scenario as “stupid money” trading, as conventional wisdom holds that one news event or headline shouldn’t sway an investor from a strategy-guided long-term investment position. The fact is, by the time the average investor reacts to overnight data, it’s likely the chance for profit is already gone.

Here’s why: Most professional day traders were likely already aware of the news, and have already priced that information into their portfolios. As the price goes up on a stock based on artificial demand, the professional traders typically step in and take the other side of the trade, knowing that in the long run, investing money will drift back to the original trade price for the stock and the professional investor will likely end up making money.

Power Hour End of Day

The last hour of the trading day may also come with high market volatility, which tends to generate more stock trading. Many professional traders tend to trade actively in the morning session and step back during mid-day trading, when volatility is lower and the market is quieter than in the first and last hours of the day.

Regular traders can perk up at the last hour of trading, where trading is typically more frequent and the size of trades generally climb as more buyers and sellers engage before the trading session closes out. Just as in the first hour of the trading day, amateur investors tend to wade into the markets, buying and selling on the day’s news.

That activity can attract bigger, more seasoned traders who may be looking to take advantage of ill-considered positions by average investors, which increases market trading toward the close.

Red Flags and Triggers to Look for During Power Hour Trading

For any investor looking to gain an advantage during power hour trading, the idea is to look for specific market news that can spike market activity and heighten the chances of making a profit in the stock market.

These “triggers” may signal an imminent power hour market period, when trading can grow more volatile.

Any Earnings Report

Publicly-traded companies are obligated to release company earnings on a quarterly basis. When larger companies release earnings, the news has a tendency to move the financial markets. Depending on whether the earnings news comes in the morning or after hours, investors can typically expect higher trading to follow. That could lead to heavier power hour trading.

News on Big “Daily Gainers”

Stock market trading activity can grow more intense when specific economic or company news pushes a single large stock — or stock sector — into volatile trading territory.

For instance, if a technology company X announces a new product release, investors may want to pounce and buy that tech stock, hoping for a significant share price uptick. That can lead to higher volume trading stock X, making the company and the market more volatile (especially later in the day), thus ensuring an active power hour trading time.

Reserve/Economic News

Major economic news, like jobs reports, consumer sentiment, inflation rates, and gross domestic product (GDP) reports, are released in the morning. Big news from the Federal Reserve typically comes later in the day, after a key speech by a Fed officer or news of an interest rate move after a Fed Open Markets Committee meeting.

Make no mistake, news on both fronts can be big market movers, and can lead to even more powerful power hour trading sessions.

Anticipation of huge economic news, like a Federal Reserve interest rate hike or the release of the U.S. government’s monthly non-farm labor report, can move markets before the actual news is released, potentially fueling an even larger trading surge after the news is released, either at the open (for government economic news) or at the end of the trading day (for Federal Reserve news).

Triple Witching Hour Events

Quarterly triple witching hours — when stock options, futures and index contracts expire on four separate Fridays during the year — historically have had a substantial impact on market activity on those Friday afternoons, in advance of the contracts expiring at the days’ end.

When options contracts involving larger companies expire, market activity on a Friday afternoon prior to closing can be especially volatile. Thus, any late afternoon power hour on a triple-witching-hour Friday can be highly active, and may be one of the largest drivers of power hour trading during the year.

The Takeaway

The concept of a stock market “power hour” is based on the increased activity at certain times of day — typically the market’s open and close. While the power hour presents opportunities for some traders, others may find it risky.

Consequently, it’s a good idea to give power hours a wide berth if you’re not familiar with trading in choppy markets, where the risk of losing money is high when power trading activity is at its highest.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

Is the power hour a good time to trade?

For sophisticated short-term traders, trading power hour stocks can be advantageous. The heightened market activity often presents a number of opportunities. For those less skilled at maximizing these short windows of opportunity, power hour trading can be highly risky.

Is the power hour more volatile?

Yes, the hallmark of the power hour, whether at the market’s open or close, is its volatility. In short, the power hour is a high-risk time in the market for most ordinary investors.

Can you make money during the power hour?

It’s possible to make money during the power hour, assuming you have the skill and the strategies to seize the opportunities presented by short-term price movements.

Photo credit: iStock/Tatiana Sviridova

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Options involve risks, including substantial risk of loss and the possibility an investor may lose the entire amount invested in a short period of time. Before an investor begins trading options they should familiarize themselves with the Characteristics and Risks of Standardized Options . Tax considerations with options transactions are unique, investors should consult with their tax advisor to understand the impact to their taxes.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Editor's Note: Options are not suitable for all investors. Options involve risks, including substantial risk of loss and the possibility an investor may lose the entire amount invested in a short period of time. Please see the Characteristics and Risks of Standardized Options.

When investors talk about hedging, it refers to a common risk-management strategy that involves taking a position with one investment to help offset the potential risk of loss in another investment.

For example, bonds and cash may be used to counterbalance potential risk exposure from the equities portion of a portfolio.

Hedging methods vary widely, depending on what the investor views as the main risk factors in their portfolio. Common hedges include derivatives, like options and futures contracts, or investments in commodities like gold or oil, or fixed-income investments.

Key Points

• Hedging is a risk-management strategy where one investment is used to offset potential loss in another investment.

• Common hedging methods include derivatives (options, futures), commodities (gold, oil), or fixed-income investments.

• Hedging acts like an insurance policy, protecting holdings in the event of risk, but it also comes with costs in time and money.

• Various hedging strategies exist, such as diversification, spread hedging, forward hedging, and more.

• Hedging is viable for retail investors, ranging from simple diversification to more complex options strategies.

What Is Hedging?

Hedging can be defined as making an investment to reduce the risks associated with another investment. For some investors, protecting a portfolio against downside risk can be as important as generating returns, whether investing online or with a brokerage.

Often, some investors may hedge to protect themselves in the event that their investments decline in value, in order to limit potential losses. While technically speaking hedging means investing in a particular security to offset the risk from a related security, there are many ways to hedge.

One common hedge is through basic diversification: choosing an investment whose price movements historically do not correlate to the main investment (e.g., when fixed-income securities are used to hedge against equities).

Also, many investors go about hedging with options contracts, purchasing securities that move in the opposite direction of the main investment.

In many ways, hedging investments works like an insurance policy. A homeowner may purchase insurance to protect their home from fire or other potential risks. That insurance policy costs money, which is an investment of sorts. So if there’s a fire, that insurance may protect the homeowner from greater losses.

Hedging is like that insurance policy. Investors trading stocks and other securities can’t protect against all risks. But with the proper hedges in place they can protect their holdings from possible risk factors. But, like insurance, those hedges cost money to make.

Hedging may also reduce an investor’s exposure to the upside of the other elements of their portfolio.

Pros & Cons of Hedging

To understand the pros and cons of hedging, consider an airline, whose fuel costs impact the company’s profitability. The airline may have a trading desk whose sole job is to buy and sell options and futures contracts related to crude oil, as a way of protecting the company against the shock of a sudden upturn in oil prices.

Pros of Hedging

The first pro of hedging for the airline is that those financial derivative instruments allow it to project its fuel costs with some degree of certainty at least a few months into the future.

The other pro of hedging comes when the price of oil skyrockets for some reason. In that case, the airline knows it can buy oil at the previously predetermined price in the oil futures contracts it owns.

Cons of Hedging

The con of hedging would be the constant ongoing expense of maintaining it. The airline has to pay for the oil futures contracts, even if it never exercises them. Futures contracts expire on a regular basis, requiring the company to continue buying them. And if fuel costs don’t go up, then it’s likely that the futures contracts the airline buys will be worthless when they expire.

The company also has to devote personnel to maintaining the portfolio of its hedges, to buy and sell the derivatives, and to periodically test the hedge to make sure it continues to protect the company as the markets shift. For the airline that represents money and talent that is diverted away from its core business.

The analogy for investors is clear. While hedges can protect an investment plan, they also come with a cost in time and money. And it’s up to each investor to determine whether the cost of a hedge is worth the protection it offers.

Hedging Examples and Strategies

There are several ways that investors can use hedging to help protect their portfolios.

Diversification

Portfolio diversification is probably the best known and most widely used risk management strategy. It relies on a broad mix of investments within a portfolio to help protect the portfolio from facing too large of a loss if one investment loses value.

A diversified portfolio will hold several distinct asset types to reduce its exposure to any single investment risk. For example, investors may balance out the risk of a stock holdings with bond securities, since bonds tend to perform better in markets where stocks struggle.

Spread Hedging

Spread hedging is a risk-management strategy employed by options traders. In this strategy, a trader will buy and/or sell two or more options contracts on the same underlying asset with the goal of limiting their losses if the price of the asset moves against them, typically in exchange for limited profit potential.

In a bull put spread, for example, a trader might purchase one put option with a lower strike price and sell another put with a high strike price with the hope of benefitting from a rise in the underlying asset’s price, while capping losses if the price falls.

Forward Hedge

Forward contracts are financial derivatives used mostly by businesses to protect themselves from changes in the value of a currency. For the purchaser, the contract effectively fixes the rate of exchange between two currencies for a period of time. The airline example discussed above is a forward hedge.

Delta Hedging

Delta hedging is a strategy used by options traders to reduce the directional risk of price movements in the security underlying the options contracts. In the strategy, the trader buys or sells options to offset investment risks and reach a delta neutral state, in which the investment is protected regardless of which way the asset price moves.

Tail Risk Hedging

Tail risk hedging refers to an array of strategies whose goal is to protect against extreme shifts in the markets. The strategies involve a close study of the major risk factors faced by a portfolio, followed by a search for the least expensive investments to protect against the most extreme of those risks.

For example, an investor overweight U.S. equities might purchase derivatives based on the Volatility Index, which tends to negatively correlate to the S&P 500 Index.

Binary Options Hedging Strategy

In a binary options hedging strategy, the investor buys both a put and a call on the same underlying security, each with a strike price that makes it possible for both options to be in the money at the same time. Binary options only guarantee a payout if a predetermined event occurs.

Forex Hedging

A forex hedge in the forex market refers to any transaction made to protect an investment from changes in currency values. As a hedge, they may be used by investors, traders and businesses. For example, since GBP/USD and EUR/USD typically have a positive correlation, you could hedge a long position in GBP/USD with a short position in EUR/USD.

Another example of forex hedging is purchasing a currency-hedged ETF. Doing so gives investors the protection of a forex hedge against the investments within their ETFs, without having to actually purchase the hedge on their own.

Hedging for Hyperinflation

Inflation hedges are those investments that have outperformed the market when inflation is a major factor in the economy. While every inflationary period is different, with various global, market and macroeconomic factors in play, investors have historically found shelter — and sometimes growth — during inflation by investing in certain assets.

Some investments that have a reputation as inflation hedges include precious metals such as gold, and commodities like oil, corn, beef, and natural gas. Other inflation hedges include alternative investments, such as REITS and real estate income.

Dollar-Cost Averaging

Some investors view dollar-cost averaging, which involves investing a set amount of money at preset intervals regardless of market performance, as a way to hedge against market volatility. That’s because dollar-cost averaging, by definition, means that you’re buying investments when they’re both high and low — and you don’t have to worry about trying to time the market.

Is Hedging Viable for Retail Investors?

Yes. While some hedging involves complicated options strategies, you can also hedge your portfolio by simply making sure that you have diversified holdings. If you’re investing to protect against certain risks, such as inflation or interest rate increases, that’s also an example of hedging.

The Takeaway

Hedges are investments, often derivatives, that help protect investors from risk. Hedging is a common strategy to use certain types of securities to offset the risk of loss from another security.

However, it’s possible to hedge some investments without investing in derivatives. Building a diversified portfolio of stocks and bonds, for example, or investing in real estate to protect against inflation risk are also examples of hedging.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

How does hedging work in simple terms?

Hedging works by counterbalancing the risk of an existing investment. For example, if you own stocks, you might use options or bonds to reduce your overall exposure to stock market volatility, thereby limiting potential downside.

What are some common methods for hedging?

Diversification is one widely used risk management strategy. Other common hedging methods include derivatives (options, futures), commodities (gold, oil), or fixed-income investments.

What is the downside of hedging?

Hedging requires time and effort to set up the appropriate hedge for your investments, and there may be associated costs as well. In addition, because hedging focuses on avoiding downside risks, it may limit a certain amount of upside.

Photo credit: iStock/Rossella De Berti

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Options involve risks, including substantial risk of loss and the possibility an investor may lose the entire amount invested in a short period of time. Before an investor begins trading options they should familiarize themselves with the Characteristics and Risks of Standardized Options . Tax considerations with options transactions are unique, investors should consult with their tax advisor to understand the impact to their taxes.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by emailing customer service at [email protected]. Please read the prospectus carefully prior to investing.

S&P 500 Index: The S&P 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. It is not an investment product, but a measure of U.S. equity performance. Historical performance of the S&P 500 Index does not guarantee similar results in the future. The historical return of the S&P 500 Index shown does not include the reinvestment of dividends or account for investment fees, expenses, or taxes, which would reduce actual returns.

Dollar Cost Averaging (DCA): Dollar cost averaging is an investment strategy that involves regularly investing a fixed amount of money, regardless of market conditions. This approach can help reduce the impact of market volatility and lower the average cost per share over time. However, it does not guarantee a profit or protect against losses in declining markets. Investors should consider their financial goals, risk tolerance, and market conditions when deciding whether to use dollar cost averaging. Past performance is not indicative of future results. You should consult with a financial advisor to determine if this strategy is appropriate for your individual circumstances.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

An investor should consider the investment objectives, risks, charges, and expenses of the Fund carefully before investing. This and other important information are contained in the Fund’s prospectus. For a current prospectus, please click the Prospectus link on the Fund’s respective page. The prospectus should be read carefully prior to investing.

Alternative investments, including funds that invest in alternative investments, are risky and may not be suitable for all investors. Alternative investments often employ leveraging and other speculative practices that increase an investor's risk of loss to include complete loss of investment, often charge high fees, and can be highly illiquid and volatile. Alternative investments may lack diversification, involve complex tax structures and have delays in reporting important tax information. Registered and unregistered alternative investments are not subject to the same regulatory requirements as mutual funds.

Please note that Interval Funds are illiquid instruments, hence the ability to trade on your timeline may be restricted. Investors should review the fee schedule for Interval Funds via the prospectus.

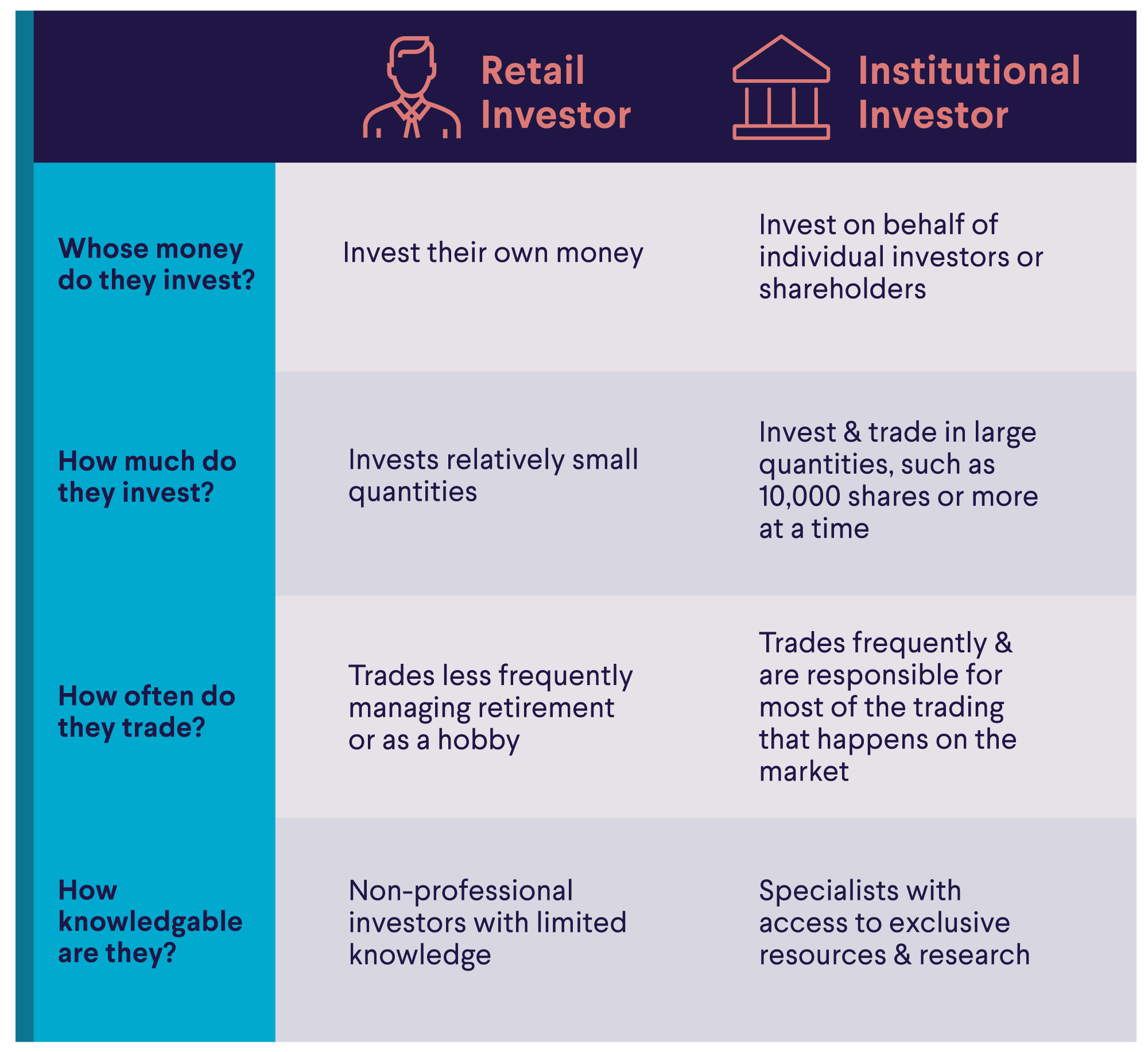

Retail investors are individuals, typically not professional, who invest their own money through a personal brokerage or retirement account. Institutional investors are financial organizations that trade investments in large quantities, on behalf of others (e.g., pension funds, mutual funds, hedge funds, and so on).

While size and scale are two of the main differences between institutional vs. retail investors, there are other distinctions. Retail investors are afforded certain legal protections; institutional investors may have the upside in terms of research and access to capital.

In addition, retail investors typically pay higher fees for investment products, compared to institutions, which generally benefit from taking larger positions.

Key Points

• Retail investors are individual investors who typically invest their own money for their personal goals.

• Institutional investors include large organizations such as banks, mutual funds, and pension funds, which invest large amounts of capital on behalf of others.

• Institutional investors place trades on a much larger scale, which can impact market movements.

• Retail investors may be impacted by institutional trades, but the reverse rarely occurs, although there can be exceptions.

• Institutional investors typically have access to more capital and proprietary data and analysis that retail investors do not.

Who Is Considered a Retail Investor?

Any non-professional individual buying and selling securities such as stocks or mutual funds and exchange traded funds (ETFs) — whether investing online or in a traditional brokerage or other type of account — is typically a retail investor.

The parent who invests in their child’s 529 college savings plan, or the employee who contributes to their 401(k) are both considered retail investors.

So, in this case the term “retail” generally refers to an individual trading on their own behalf, not on behalf of a larger pool of investors. Retail here references the purchase and selling of investments in relatively small quantities.

Who Is Classified as an Institutional Investor?

By comparison, institutional investors make investment decisions on behalf of large pools of individual investors or shareholders. In general, institutional investors trade in large quantities, such as trading stocks by 10,000 shares or more at a time.

The professionals who do this large-scale type of investing typically have access to investments not available to retail investors (such as special classes of shares that come with different cost structures). By virtue of their being part of a larger institution, this type of investor usually has a larger pool of capital to buy, trade, and sell with.

Institutional investors are responsible for most of the trading that happens on the market. Examples of institutional investors include commercial banks, pension funds, mutual funds, hedge funds, endowments, insurance companies, and real estate investment trusts (REIT).

What Are the Differences Between Institutional Investors vs Retail Investors?

The main differences between institutional and retail investors include:

• Institutional investors invest on behalf of a large number of constituents (e.g., a mutual fund or municipal pension fund); retail investors are individuals who invest for themselves (e.g., in an IRA or a self-directed brokerage account).

• Size (large institutions vs. individuals) and scale of investments.

• Institutional investors typically have access to professional research and industry resources.

• Retail investors are protected by certain regulations that don’t apply to institutional investors.

Institutional Investors

Retail Investors

Professionals and large companies

Non-professional individuals

Invest in large quantities

Invest in small quantities

Trades less frequently; may manage retirement or invest as a hobby

Invest for themselves

Access to industry-level sources, research

DIY

Access to preferred share classes and pricing

Access to retail shares and pricing

There are very few similarities between institutional vs. retail investors, except that both parties tend to seek returns while minimizing risk factors where possible.

Do Institutional or Retail Investors Get the Highest Returns?

There are no crystal balls on Wall Street, as they say, so there’s no guaranteed way to predict whether institutional investors always get higher returns vs. retail investors.

That said, some institutional investors may have the edge in that they have access to industry-level research, as well as powerful technology and computer algorithms that typically enable them to make faster trades and more profitable calculations.

Does that mean institutional investors always come out ahead? In fact, retail investors who have a longer horizon also have a chance at substantial returns over time, although there are no guarantees on either side.

Get up to $1,000 in stock when you fund a new Active Invest account.*

Access stock trading, options, alternative investments, IRAs, and more. Get started in just a few minutes.

*Customer must fund their Active Invest account with at least $50 within 45 days of opening the account. Probability of customer receiving $1,000 is 0.026%. See full terms and conditions.

How Many Retail Investors Are There?

In the U.S., it’s fairly common to be a retail investor. About 62% of Americans say they own stock, according to a 2025 Gallup poll, meaning they own individual stocks, stock mutual funds, or they hold stock in a self-directed 401(k) or IRA.

Examples of retail investors include people who manage their retirement accounts online (e.g., an IRA) and those who trade stocks as a hobby.

Because individual investors are generally thought to be more prone to emotional behavior than their professional counterparts (and typically don’t have access to the resources and research of larger institutions), they may be exposed to higher levels of risk. Thus the Security Exchange Commission (SEC) provides certain protections to retail investors.

For example, the 2019 Regulation Best Interest rule states that broker-dealers are required to act in the best interest of a retail customer when making a recommendation of a securities transaction or investment strategy. This federal rule is intended to ensure that broker-dealers aren’t allowed to prioritize their own financial interests at the expense of the customer.

Another protection provided to retail investors is that investment advisors and broker-dealers must provide a relationship summary that covers services, investment fees and costs, conflicts of interest, legal standards of conduct, and more to new clients.

Types of Institutional Investors

The most common institutional investors are listed below.

1. Commercial Banks

Commercial banks are the “main street” banks many people are familiar with, such as Wells Fargo, Citibank, JP Morgan Chase, Bank of America, TD Bank, and countless others. Along with providing retail banking services, such as savings accounts and checking accounts, large banks are also institutional investors.

These large corporations have entire teams dedicated to investing in different markets: e.g., global markets, bond markets, socially responsible investing, and so on.

2. Endowment Funds

Typically connected with universities and higher education, endowment funds are often created to help sustain these nonprofit organizations. Churches, hospitals, nonprofits, and universities generally have endowment funds, whose funds often derive from donations.

Endowment funds generally come with certain restrictions, and have an investment policy that dictates an investment strategy for the manager to follow. This might include stipulations about how aggressive to be when trying to meet return goals, and what types of investments are allowed (some endowment funds avoid controversial holdings like alcohol, firearms, tobacco, and so on).

Another component is how withdrawals work; often, the principal amount invested stays intact while investment income is used for operations or new constructions.

3. Pension Funds

Pension funds generally come in two flavors:

• Defined contribution plans, such as 401(k)s or 403(b)s, where employees contribute what they can to these tax-deferred accounts.

• Defined benefit plans, or pensions, where retirees get a fixed income amount, regardless of how the fund does.

Employers that offer defined-benefit pension plans are becoming less common in the U.S. Where they do exist, they’re often linked to labor unions or the public sector: e.g., a teachers union or auto workers union may offer a pension.

Public pension funds follow the laws defined by state constitutions. Private pension plans are subject to the Employee Retirement Income Security Act of 1974 (ERISA); this act defines the legal rights of plan participants.

As for how a pension invests, it depends. ERISA does not define how private plans must invest, other than requiring that the plan sponsors must be fiduciaries, meaning they put the financial interest of the account holders first.

4. Mutual Funds

As defined by the Securities and Exchange Committee (SEC), mutual funds are companies that pool money from many investors and invest in securities such as bonds, stocks, and short-term debt. Mutual funds are thus considered institutional investors, and are known for offering diversification, professional management, affordability, and liquidity.

Typical mutual fund offerings include money market funds, bond funds, stock funds, index funds, actively managed funds, and target date funds.

The last category here is often designed for retail investors who are planning for retirement. The asset mix of these target date funds, sometimes known as target funds or lifecycle funds, shifts over time to become more conservative as the investor’s target retirement date approaches.

5. Hedge Funds

Like mutual funds, hedge funds pool money from investors and place it into securities and other investments. The difference between these two types of funds is that hedge funds are considered private equity funds, are considered high-risk vehicles, and are only available to accredited investors.

Because hedge funds use strategies and investments that chase higher returns, they also carry a greater risk of losses — similar to high-risk stocks. In general, hedge funds also have higher fees and higher minimum investment requirements. So, they tend to be more popular with wealthier investors and other institutional investors.

6. Insurance Companies

Perhaps surprisingly, insurance companies can also be institutional investors. They might offer products such as various types of annuities (fixed, variable, indexed), as well as other life insurance products which are invested on behalf of the investor, e.g. whole life or universal life insurance policies.

The Takeaway

Institutional investors may be larger, more powerful, and run by professionals — whereas retail investors are individuals who aren’t trained investment experts — but it’s important to remember that these two camps can and do overlap. Institutional investors that run pension funds, mutual funds, and insurance companies, for example, serve retail investors by investing their money for retirement and other long-term goals. While retail investors still have the ability to invest their own money for their own goals.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

What are the different types of investors?

Institutional investors are big companies with teams of professional investment managers who invest other people’s money. Retail investors are individuals who typically manage their own investment (e.g. for retirement or college savings).

What percentage of the stock market is made up of institutional investors?

The vast majority of stock market investors are institutional investors. Because they trade on a bigger scale than retail investors, institutional trades can impact the markets.

Are institutional or retail investment strategies better?

Institutional investors have access to more sophisticated research and technology compared with retail investors. Thus their strategies may be considered more complex. But it’s hard to compare outcomes, as both groups are exposed to different levels of risk.

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by emailing customer service at [email protected]. Please read the prospectus carefully prior to investing.

Mutual Funds (MFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or clicking the prospectus link on the fund's respective page at sofi.com. You may also contact customer service at: 1.855.456.7634. Please read the prospectus carefully prior to investing.Mutual Funds must be bought and sold at NAV (Net Asset Value); unless otherwise noted in the prospectus, trades are only done once per day after the markets close. Investment returns are subject to risk, include the risk of loss. Shares may be worth more or less their original value when redeemed. The diversification of a mutual fund will not protect against loss. A mutual fund may not achieve its stated investment objective. Rebalancing and other activities within the fund may be subject to tax consequences.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

This article is not intended to be legal advice. Please consult an attorney for advice.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

Portfolio diversification involves investing money across a range of different asset classes — such as stocks, bonds, and real estate — rather than concentrating all of it in one asset class. The idea is that by diversifying the assets in your portfolio, an investor may potentially offset a certain amount of investment risk.

Building a diversified portfolio is one financial strategy an investor might use. Read on to learn how it works, why it’s important to diversify investments, and how it might fit into an individual’s financial plan.

Key Points

• Portfolio diversification involves spreading investments across different asset classes, industries, sectors, and geographic locations.

• Diversification may potentially help manage a certain amount of risk, especially unsystematic risk.

• Investors’ risk tolerance, financial goals, and time horizon may help determine portfolio diversification.

• Assets in a diversified portfolio might include domestic stocks, international stocks, bonds and other fixed-income assets, and cash or cash equivalents.

What Is Portfolio Diversification

Portfolio diversification refers to spreading the investments in a portfolio across different asset classes, industries, company sizes, sectors, and more, in an effort to potentially reduce investment risk.

To understand this aspect of portfolio management, it helps to know about the two main types of risk: systemic risk and unsystematic risk.

• Systematic risk, or market risk, is caused by widespread events like inflation, geopolitical instability, interest rate changes, or even public health crises. Investors can’t manage systematic risk through diversification, however; it’s part of the investing landscape.

• Unsystematic risk is unique to a particular company, industry, or place. Let’s say, for example, extreme weather threatens a particular crop, causing prices in that sector to drop. This is an unsystematic risk.

While investors typically can’t do much about systematic risk, portfolio diversification might help with unsystematic risk. That’s because if an investor has different holdings, even if one asset or sector is hit by a negative event, others could remain relatively stable. So while they might see a dip in part of their portfolio, other sectors could act as balance to keep returns steady.

It’s impossible to completely protect against the possibility of loss — risk is inherent in investing. But building a portfolio that’s well diversified may help reduce some risk exposure because an investor’s money is distributed across areas that aren’t as likely to react in the same way to the same occurrence.

💡 Quick Tip: All investments come with some degree of risk — and some are riskier than others. Before investing online, decide on your investment goals and how much risk you want to take.

Get up to $1,000 in stock when you fund a new Active Invest account.*

Access stock trading, options, alternative investments, IRAs, and more. Get started in just a few minutes.

*Customer must fund their Active Invest account with at least $50 within 45 days of opening the account. Probability of customer receiving $1,000 is 0.026%. See full terms and conditions.

Why Is It Important to Diversify Your Investments?

Diversification potentially benefits investors on several levels when trading stocks and other investments. Diversification spreads money across different investments in a portfolio. That way, if one investment loses value, other investments might help offset the losses and balance things out.

Diversification may also potentially help build wealth over the long-term.

The Role of Diversification in Managing Risk

Every portfolio carries some degree of risk. Diversification may help manage that risk to some degree.

How diversification may strengthen an investor’s portfolio begins with balancing the individual’s risk tolerance against their risk capacity.

Risk tolerance is the amount of risk an investor feels comfortable with. Risk capacity is the level of risk they need to take to meet their investment goals. Too much risk could set an investor up for potential losses, while taking too little risk could mean missing out on investment growth.

Here are some of the key areas where diversification plays a role in risk management.

• Asset mix. Including a mix of assets in a portfolio allows investors to avoid the mistake of putting all their eggs in one basket. The idea is that if one area of their portfolio underperforms, their other investments might help balance things out.

• Geographic variation. Investing in both domestic and international markets may help investors tap into market trends across borders. While one country’s economy might not be doing well, another may be thriving. Diversifying geographically could be a way to help manage risks associated with location-specific downturns.

• Stabilization. Diversification may help with volatility if the market gets bumpy. For example, holding assets that have varying levels of correlation to stocks may offer some insulation against broad pricing swings or more sustained downturns. Bonds, for instance, typically have low correlation to stocks. By owning both, a portfolio may potentially experience more stability and less volatility.

Taking a risk tolerance quiz can help to determine an individual’s risk tolerance. An investor can then consider what kind of risk capacity they’ll need to help reach their long-term goals.

Those that favor a conservative investing approach might choose investments such as bonds, blue chip stocks, and cash equivalents. Investors that are comfortable with a more aggressive approach may opt for a mix of growth-focused investments that are higher risk, but may have a higher potential reward.

How to Build a Diversified Portfolio: 5 Key Asset Classes

To build a diversified portfolio, an investor can think about asset allocation, based on available capital, risk tolerance, and time horizon (meaning the amount of time they have to invest) and spreading out investments within each asset class. Here are five options to consider.

1. Domestic Stocks (U.S. Equities)

Domestic stocks are shares in companies that operate in the country in which an investor lives. Examples of U.S. domestic stocks include Apple, Google, and Costco.

Investing in domestic equities can be convenient, since an investor can buy shares on a public stock exchange. And they may already be familiar with a company’s products or services.

Owning individual stocks does have risks, however. Another option is to invest in ETFs. An ETF (exchange-traded fund) offers exposure to multiple stocks, bonds, and other investments in a single basket. Unlike traditional mutual funds, ETFs trade on a stock exchange like stocks and tend to be more cost-effective.

2. International Stocks (Global Equities)

Global equities are stocks from companies that operate outside an investor’s home country. Adding international stocks to a portfolio may potentially help with diversification since markets and economies don’t always move in the same direction at once.

Established markets may offer stability and predictability. Emerging markets might yield the potential for higher growth. But both have risks that are important to weigh.

With established markets, for example, there could be a ripple effect that when one country experiences a marked shift that creates shifts in other markets. A downturn in the U.S. stock market, for instance, could trigger price drops in European or Asian stock exchanges. Emerging countries, meanwhile, may be more susceptible to political instability or currency risk.

3. Bonds and Other Fixed-Income Assets

Bonds are issued by corporations and government entities. When an individual invests in a bond, they’re essentially giving the bond issuer a loan. In exchange, the issuer agrees to pay them a set interest rate on the money.

Bonds are a type of fixed-income investment, since they’re designed to provide predictable income to investors. Treasury bills, Treasury Inflation Protected Securities (TIPS), and mortgage-backed securities (MBS) are other examples of fixed-income investments.

Including bonds and other fixed-income options in a portfolio may help with diversification. These assets are typically considered to be lower risk than stocks. However, that doesn’t mean returns on bonds are guaranteed. It’s possible to lose money in bonds if the issuer defaults, for example.

4. Real Estate (e.g., REITs)

Real estate is another asset some investors might consider. Real estate investment trusts (REITs) and/or real estate ETFs are one way to invest in property without the hands-on requirements of ownership.

A REIT is a legal entity that owns and operates rental properties. REITs may own a single type of property or several. Some common REIT property types include:

• Apartment buildings

• Student housing

• Healthcare facilities

• Office space

• Retail space

• Storage space

• Warehouse space

REITS are required to pay out 90% of their taxable income to shareholders as dividends. Real estate ETFs primarily invest in REITs, but they can hold other real estate-related investments as well.

5. Alternative Investments and Commodities

Alternative investments are investments that are not traditional asset classes such as stocks or bonds. Examples of alternative investments include:

• Fine art

• Fine wines

• Antique or collectible cars

• Private equity

• Private credit

Commodities like oil, what, or gain, are also a type of alternative investment.

Alternative investments may offer the possibility of higher returns, but they’re highly risky and speculative.

What Does a Diversified Portfolio Look Like? (Examples)

A diversified portfolio example can help an investor visualize how their investments might pay off over time. For instance, the 60-40 rule is one basic rule of thumb for asset allocation. With this strategy, an individual invests 60% of their portfolio in equities and 40% in fixed income and cash. Here’s what that method looks like.

That’s just one example. A portfolio can contain a broader mix of assets that includes stocks, bonds, alternative assets, REITs, and much more.

An investor’s risk tolerance also typically influences what their portfolio might look like. Here are some examples of conservative, moderate, and aggressive portfolios.

Example of a Conservative Portfolio

A conservative portfolio might generally have a higher proportion of bonds, fixed-income, and cash investments compared to stocks. It might look something like this:

• 30% stocks

• 60% bonds

• 10% cash

This type of portfolio typically carries a lower degree of risk, but it may limit growth potential.

Example of a Moderate Portfolio

The 60/40 portfolio described above is an example of what a model portfolio might look like. An investor with a moderate portfolio might also choose a different mix or percentage of stocks and bonds, tailored to their needs and risk tolerance.

For instance, that might look like:

• 50/50 split, with half the money in stocks and half in bonds/fixed-income

• 70/30 split, with more devoted to stocks and less invested in bonds

Moderate portfolios aim to find a balance between riskier investments that can deliver growth, and safer, more stable holdings.

Example of an Aggressive Portfolio

An aggressive portfolio is typically more heavily weighted toward stocks. For example, such a portfolio may be composed of:

• 85% stocks

• 10% bonds/fixed-income

• 5% cash

This is the type of portfolio that may be preferred by those who are comfortable taking on more risk in exchange for a chance to potentially earn higher returns.

The Easiest Ways to Start Diversifying

When an investor is ready to start diversifying their portfolio, there are a couple of options they might want to consider to help simplify the process.

Using All-in-One ETFs or Mutual Funds

ETFs and mutual funds are a collection of multiple investments. Rather than choosing stocks or bonds individually, with an ETF or mutual fund an investor could invest in several of them all at once. ETFs are traded like stocks, while mutual funds settle once a day at the close of the market. Both assets carry expense ratios, which determine the annual cost of owning the fund.

An index fund is a type of mutual fund that attempts to mimic the performance of a specific stock index. For example, there are funds that track the S&P 500. In this case, how well the fund performs is ultimately tied to the movements of its underlying index.

Knowing the underlying investments in ETFs or mutual funds might help prevent overweighting the asset allocation, which could happen if an individual invests in multiple funds that hold the same kind of investments.

Using an Automated Investing Service

Another option some investors might want to consider is using a robo-advisor to do portfolio diversification. With an automated investing platform, individuals can typically get a customized portfolio that’s tailored to their age, risk tolerance, and goals.

In addition, automatic rebalancing may help investors maintain the appropriate level of diversification. Rebalancing means buying and selling assets to keep the allocation aligned with an investor’s original targets.

Automated investing is not for everyone, and it may have limitations such as less control and fewer choices. However, some investors might find it to be a convenient way to diversify without being completely hands-on.

What Are the Main Pros and Cons of Diversification?

Diversification offers advantages and disadvantages for investors to consider. Here are two specific factors to keep in mind.

Advantage: Smoothing Out a Portfolio’s Returns

One potential benefit of diversification is that it may help reduce an investor’s overall level of risk. It may possibly create a smoother experience for investors during times of market volatility by providing balance through different asset classes, sectors, and regions.

Disadvantage: Potentially Limiting Your Upside

A possible drawback to diversification includes the fact that returns may be limited by a more risk-averse approach. Also, diversification does not help protect against all risk, especially market-specific risk. And diversification does not eliminate risk.

The Takeaway

Portfolio diversification is one of the key tenets of long-term investing. Instead of putting money into one investment or a single asset class like stocks or bonds, diversification spreads it out across a range of securities. Investors may vary their investments in a way that matches their goals and tolerance for risk.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

What is an example of a well-diversified portfolio?

An example of a well-diversified portfolio is one that fits an investor’s financial situation, goals, risk tolerance, and time horizon. For example, a conservative portfolio might have 30% stocks, 60% bonds, and 10% cash. A moderate portfolio may contain a 50%-50% split of stocks and fixed assets including bonds. And an aggressive portfolio might have 85% stocks, 10% fixed assets, and 5% cash. But again, these are just examples.

What are the dangers of over-diversifying your portfolio?

An over-diversified portfolio might lead to owning too many similar or overlapping investments, such as too many mutual funds that are similar in terms of their holdings. Over-diversification may also reduce a portfolio’s returns without meaningfully reducing risk.

When should you diversify your portfolio?

While there is no one right answer to when to diversify, an investor might decide to diversify their portfolio as soon as they start investing, for example. They might spread out their investment over different asset classes, industries, company sizes, sectors, regions, and so on. Investors can check their asset allocation at regular intervals to make sure they are properly diversified in accordance with their risk tolerance, time horizon, and goals.

Does diversification guarantee I won’t lose money?

No. Diversification is not a guarantee that you won’t lose money. Investing is inherently risky, and there is no strategy that eliminates the risk. A diversified portfolio might offer a way to help manage some risk, but it cannot eliminate risk.

How many stocks should I own to be diversified?

There’s no specific number of stocks an investor should own to be diversified. How many stocks an individual chooses to hold can depend on their risk tolerance, investment style, goals, and time horizon among other factors.

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Mutual Funds (MFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or clicking the prospectus link on the fund's respective page at sofi.com. You may also contact customer service at: 1.855.456.7634. Please read the prospectus carefully prior to investing.Mutual Funds must be bought and sold at NAV (Net Asset Value); unless otherwise noted in the prospectus, trades are only done once per day after the markets close. Investment returns are subject to risk, include the risk of loss. Shares may be worth more or less their original value when redeemed. The diversification of a mutual fund will not protect against loss. A mutual fund may not achieve its stated investment objective. Rebalancing and other activities within the fund may be subject to tax consequences.

Exchange Traded Funds (ETFs): Investors should carefully consider the information contained in the prospectus, which contains the Fund’s investment objectives, risks, charges, expenses, and other relevant information. You may obtain a prospectus from the Fund company’s website or by emailing customer service at [email protected]. Please read the prospectus carefully prior to investing.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

S&P 500 Index: The S&P 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S. It is not an investment product, but a measure of U.S. equity performance. Historical performance of the S&P 500 Index does not guarantee similar results in the future. The historical return of the S&P 500 Index shown does not include the reinvestment of dividends or account for investment fees, expenses, or taxes, which would reduce actual returns.

An investor should consider the investment objectives, risks, charges, and expenses of the Fund carefully before investing. This and other important information are contained in the Fund’s prospectus. For a current prospectus, please click the Prospectus link on the Fund’s respective page. The prospectus should be read carefully prior to investing.

Alternative investments, including funds that invest in alternative investments, are risky and may not be suitable for all investors. Alternative investments often employ leveraging and other speculative practices that increase an investor's risk of loss to include complete loss of investment, often charge high fees, and can be highly illiquid and volatile. Alternative investments may lack diversification, involve complex tax structures and have delays in reporting important tax information. Registered and unregistered alternative investments are not subject to the same regulatory requirements as mutual funds.

Please note that Interval Funds are illiquid instruments, hence the ability to trade on your timeline may be restricted. Investors should review the fee schedule for Interval Funds via the prospectus.

Fund Fees

If you invest in Exchange Traded Funds (ETFs) through SoFi Invest (either by buying them yourself or via investing in SoFi Invest’s automated investments, formerly SoFi Wealth), these funds will have their own management fees. These fees are not paid directly by you, but rather by the fund itself. these fees do reduce the fund’s returns. Check out each fund’s prospectus for details. SoFi Invest does not receive sales commissions, 12b-1 fees, or other fees from ETFs for investing such funds on behalf of advisory clients, though if SoFi Invest creates its own funds, it could earn management fees there.

SoFi Invest may waive all, or part of any of these fees, permanently or for a period of time, at its sole discretion for any reason. Fees are subject to change at any time. The current fee schedule will always be available in your Account Documents section of SoFi Invest.

– Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

NBBO — the National Best Bid and Offer — is a quote available marketwide that represents the tightest composite spread for a security, e.g., the highest bid price and the lowest ask price for that security trading on various exchanges.

The NBBO is a regulation put in place by the Securities and Exchange Commission (SEC) that requires brokers who are working on behalf of clients to execute a trade at the best available ask price, and the best available bid price.

Brokers must guarantee at least the NBBO to their clients at the time of a trade, per SEC rules.

Key Points

• The National Best Bid and Offer (NBBO) is a marketwide quote for the highest bid price and the lowest ask price for a security across exchanges.

• The SEC enacted the NBBO regulation to ensure brokers execute trades for clients at the best available bid and ask prices (the bid-ask spread).

• The bid-ask spread is the difference between the price an investor is willing to buy (bid) and the price a seller is willing to sell (ask).

• Securities Information Processors (SIPs) continuously process bid and ask prices to calculate and update the NBBO.

• There can be a slight lag in real-time data due to the high volume of transactions, which the SEC addresses with intermarket sweep orders (ISO).

How Does “Bid vs Ask” Work in the Stock Market

In order to understand NBBO, investors need to understand the bid-ask price of a security, such as a stock. This is also known as the spread (two of many terms investors and traders should know). If an investor is “bidding,” they’re looking to buy. If they’re “asking,” they’re looking to sell. It may be helpful to think of it in terms of an “asking price,” as seen in real estate.

The average investor or trader will typically see the bid or ask price when looking at prices for different securities. Most of the bid-ask action takes place behind the scenes, and it’s happening fast, landing on an average price. These are the prices represented by stock quotes.

That price is the value at which brokers or traders are required to guarantee to their customers when executing orders. NBBO requires brokers to act in the best interest of their clients.

The National Best Bid and Offer (NBBO) is effectively a consolidated quote of the highest available bid and the lowest available ask price of a security across all exchanges. NBBO was created by the SEC to help ensure that brokers offer customers the best publicly available bid and ask prices when investors buy stocks online or through a traditional brokerage.

NBBO Example

Let’s run through a quick example of how the NBBO might work in the real world.

Let’s suppose that a broker has a few clients that want to buy stock:

• Buyer 1 puts in an order to the broker to buy shares of Company X at $10

• Buyer 2 puts in an order to the broker to buy shares of Company X at $10.50

• Buyer 3 puts in an order to the broker to buy shares of Company X at $11

Remember, these are “bids” — the price at which each client is willing to purchase a share of Company X.

On the other side of the equation, we have another broker with two clients that want to sell their shares of Company X, but only if the price reaches a certain level:

• Client 1 wants to sell their shares of Company X if the price hits $12

• Client 2 wants to sell their shares of Company X if the price hits $14

In this example, the NBBO for Company X is $11/$12. Why? Because these are the best bid vs. ask prices that were available to the brokers at the time. This is, on a very basic level, how calculating the NBBO for a given security might work.

Because the NBBO is updated constantly through the day with offers for stocks from a number of exchanges and market players, things need to move fast.

Most of the heavy lifting in NBBO calculations is done by Securities Information Processors (SIPs). SIPs connect the markets, processing bid and ask prices and trades into a single data feed. They were created by the SEC as a part of the Regulation National Market System (NMS).

There are two SIPS in the U.S.: The Consolidated Tape Association (CTA) , which works with the New York Stock Exchange, and the Unlisted Trading Privileges (UTP) , which works with stocks listed on the Nasdaq exchange.

The SIPS crunch all of the numbers and data to keep prices (NBBO) updated throughout the day. They’re incredibly important for traders, investors, brokers, and anyone else working in or adjacent to the markets.

Is NBBO Pricing Up to Date?

The NBBO system may not reflect the most up-to-date pricing data. Bid, ask, and transaction data is changing every millisecond. For high-frequency traders that are making fast and furious moves on the market, these small price fluctuations can cost them.

To make up for this lag time, the SEC allows trading via intermarket sweep orders (ISO), letting an investor send orders to multiple exchanges in order to execute a trade, regardless of whether a price is the best nationwide.

The Takeaway

NBBO represents the crunching of the numbers between the bid-ask spread of a security, and it’s the price you’ll see listed on a financial news network or stock quote.

The NBBO adds some legal protection for investors, effectively forcing brokers to execute trades at the best possible price for their clients.

Invest in what matters most to you with SoFi Active Invest. In a self-directed account provided by SoFi Securities, you can trade stocks, exchange-traded funds (ETFs), mutual funds, alternative funds, options, and more — all while paying $0 commission on every trade. Other fees may apply. Whether you want to trade after-hours or manage your portfolio using real-time stock insights and analyst ratings, you can invest your way in SoFi's easy-to-use mobile app.

Invest with as little as $5 with a SoFi Active Investing account.

FAQ

What does NBBO mean in trading?

The National Best Bid and Offer (NBBO) is a marketwide quote for the highest bid price and the lowest ask price available for a security, across exchanges. That means it’s a composite or consolidated quote that ensures investors are getting the best available price for a security.

What is Level 2?

Level 2 is a subscription-based service offered by Nasdaq that gives traders access to live trading data from the exchange, including bid-ask spreads and order sizes from market makers. Level 2 offers more in-depth information about pricing than NBBO, which is part of a Level 1 trading screen.

What is the advantage of NBBO?

First and foremost, NBBO helps protect investors, by ensuring the tightest spreads for securities prices. As such, NBBO also promotes market transparency and competition.

Photo credit: iStock/g-stockstudio

INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

SoFi Invest is a trade name used by SoFi Wealth LLC and SoFi Securities LLC offering investment products and services. Robo investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser. Brokerage and self-directed investing products offered through SoFi Securities LLC, Member FINRA/SIPC.

For disclosures on SoFi Invest platforms visit SoFi.com/legal. For a full listing of the fees associated with Sofi Invest please view our fee schedule.

Disclaimer: The projections or other information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

This article is not intended to be legal advice. Please consult an attorney for advice.