How to Refinance Student Loans as an International Student

Refinancing student loans can help students save money and pay back their loan faster. However, for international students without a credit history in the U.S., refinancing options are limited. If you’re considering refinancing your student loans as an international student, it’s important to know how the process works.

This guide on student loan refinance for international students will walk you through it.

Table of Contents

Key Points

• International students can refinance student loans through select lenders, but eligibility depends on visa type and status.

• Adding a U.S. citizen or permanent resident cosigner to the loan may improve approval chances and help secure a lower interest rate.

• Refinancing doesn’t always guarantee a lower rate since approval depends on credit history and income.

• Some lenders allow you to check potential rates with a soft credit pull, avoiding an impact on your credit score.

How Refinancing Student Loans Works

Student loan refinancing is the process of replacing your current student loans with a new loan that has one monthly payment. You can refinance both private student loans and federal student loans, potentially saving money and time as you pay off your debt.

Student loan refinancing companies like SoFi offer fixed and variable interest rates that may be lower than what you’re currently paying on your student loans.

With student loan refinancing, you can also choose from various student loan repayment options and terms, allowing you to pay off your loans as quickly as your budget allows. The shorter your repayment period, the more you’re likely to save on interest, while a longer repayment term typically means you pay more interest over the life of the loan.

As you consider your strategy for paying off your student loan debt, refinancing can be a crucial element in helping you achieve your goal.

Another term you may hear as you’re exploring the idea of refinancing is “consolidation.” The terms are sometimes used interchangeably, but they are not the same thing. With student loans, consolidation is generally associated with federal loans through the Federal Direct Loan Consolidation Program, while refinancing is typically done through a private lender.

Recommended: Can International Students Get Student Loans?

Take control of your student loans.

Ditch student loan debt for good.

Where to Refinance Student Loans for International Students

When you’re an international student, it’s not always easy to know where to go to refinance your student loan. Many lenders require you to be a U.S. citizen or permanent resident to be eligible for international student loan refinance, but fortunately, some companies provide more flexibility and may offer such options as student loans for H-1B visa holders.

For instance, SoFi as well as MPOWER offer student loan refinance for international students. SoFi considers U.S. citizens, permanent residents, and people who hold a J-1, H-1B, E-2, E3, O-1, or l-1 visa (as of the date of this article).

If you’re a permanent resident, you’ll need to either have at least two years left until your status expires to refinance student loans for international students. And if you’re a visa holder, you’ll need to have at least two years left before your status expires, or you’ve applied for permanent residency.

That said, qualifying based on your citizenship, resident, or visa status doesn’t necessarily mean you qualify based on all criteria. Student loan refinancing lenders also typically have credit and income requirements.

This means that if you don’t have an established credit history — which is not always the case for international students — you may have a tough time getting approved on your own.

If this is your situation, it might be worth getting a student loan refinancing cosigner, such as a trusted family member or friend who is a U.S. citizen or permanent resident, to apply with you to help strengthen the creditworthiness of your application. This can be helpful because a cosigner acts as a backup for your application, and they are also legally obligated to repay the loan if you can’t. Even if you do qualify to refinance your student loans on your own, a co-signer could help you get a lower interest rate.

To help improve your chances of getting approved for international student loan refinance with more favorable terms, such as a low rate, it’s a good idea to choose a co-signer who has a stellar credit history and a solid income.

Eligibility Requirements for International Students

Refinancing eligibility requirements for international students can vary by lenders. However, there are some specific criteria most lenders look for.

Credit Score and Financial History

To be eligible for student loan refinance, an international student needs to have a solid credit history. Lenders generally perform a credit check on borrowers before deciding whether to give them a loan. They check the borrower’s credit score and credit report to see if they have made loan and credit card payments, which helps them assess whether the borrower can repay a refinance loan.

Most international students don’t have a credit history in the U.S. Yet most forms of borrowing, including credit cards, typically require individuals to be U.S. citizens or permanent residents. That makes it difficult to get credit. That’s why having a creditworthy cosigner on the loan can be helpful.

Lenders may also consider your income when deciding whether to give you a loan. They want to see that you have a steady income that’s high enough to make loan payments. Again, a creditworthy cosigner with a steady and sufficient income may help bolster your chances of getting a refinance loan.

Consigner Requirements and Options

When choosing a cosigner, keep in mind that they, too, will need to meet certain requirements from the lender. This generally includes:

• Being a U.S. citizen or a permanent resident

• A Social Security number

• Good to excellent credit (a good credit score is considered to be above 670)

• A stable job and a steady income

It’s important for the cosigner to understand that they are taking equal responsibility along with the primary borrower for repaying the loan. Any late or missed payments could harm their credit. Make sure the person you choose as your cosigner is someone you trust, and that they are willing to take on the responsibilities — and possible risk — involved.

Two Things to Consider Before Refinancing Your Student Loans

Refinancing might not be the right option for everyone. Here are three things to think about before you make your decision:

You May Not Qualify for a Lower Rate

Your eligibility and student loan interest rate are based on several factors, including your credit history and income. As such, there’s no guarantee you’ll get approved for a lower interest rate than what you’re currently paying, even with a co-signer.

Also, if you already have a relatively low interest rate with your current lender, you may have a hard time getting an even lower rate.

Fortunately, some lenders, including SoFi, allow you to check your rate before you officially apply to refinance. This is done with a soft credit check, which doesn’t impact your credit score.

Refinancing Is Just One Piece of the Puzzle

As you think through your student loan repayment strategy, keep in mind that refinancing isn’t the end of the line. Once you complete the process of refinancing your loans, it’s important to make sure you’re paying down your debt.

For example, consider creating a budget and looking for ways to put extra cash toward your student loan payments each month. If you get some extra money — a chunk of cash for your birthday, say — you can put that toward your loan payments as well.

Additionally, you could go with a shorter repayment period to save even more time and money on your debt. Just be aware that a shorter repayment period means your monthly payments will be higher.

Pros and Cons of Refinancing as an International Student

Refinancing your student loans as an international student could be a way to help manage your monthly payments. But there are advantages and disadvantages to carefully consider before moving ahead.

Benefits of Refinancing

The pros of refinancing student loans include:

• A lower interest rate: If they can qualify, a lower interest rate can save borrowers money on the amount of interest they pay over the life of the loan. They could potentially save thousands of dollars.

• Lower monthly payments: With more flexible loan terms, a borrower could lower monthly payments by extending the loan term. However, with a longer repayment term, they will pay more in interest over the life of the loan.

• Repayment is easier to manage: With refinancing, a borrower has just one loan to keep track of and pay each month, rather than multiple loans. This can simplify the repayment process.

Potential Drawbacks to Keep in Mind

There are several disadvantages to refinancing, such as:

• Refinancing as an international student may be challenging: Many lenders don’t offer student loan refinancing to international students. Those that do typically offer refinancing to international borrowers with certain types of visas or those with permanent residency status.

• A cosigner may be required: Many international students don’t have a credit history in the U.S, which is something lenders look for. In that case, a creditworthy cosigner may be needed to secure refinancing.

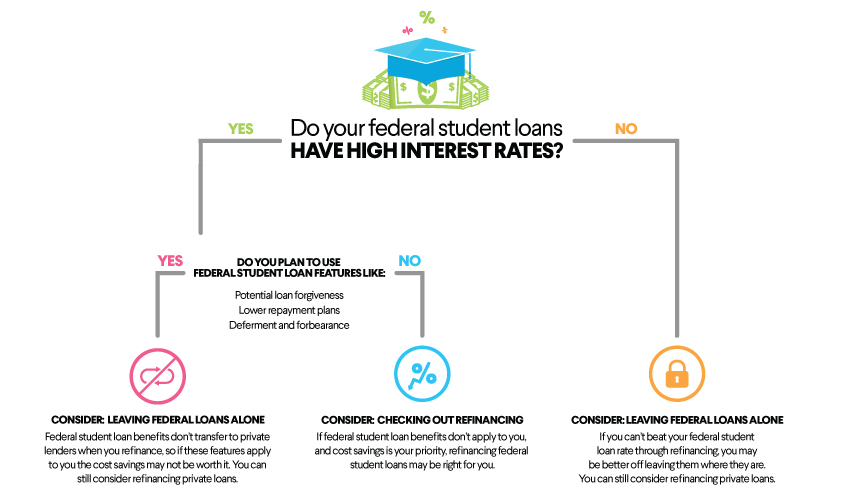

• Refinancing federal student loans makes them ineligible for federal benefits: While both federal and private student loans can be refinanced, refinancing federal loans means that borrowers no longer have access to federal programs and protections, such as income-driven repayment plans and federal deferment. (Although federal student loans are not typically available to international students, some international students who are permanent residents of the U.S. or have certain types of visas may be eligible for them.)

The Takeaway

If you’re considering refinancing student loans as an international student, be sure to check your eligibility requirements with private lenders. If you don’t have a strong credit history, consider adding a co-signer who is a U.S. citizen or permanent resident to strengthen your refinance loan application.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

FAQ

What lenders refinance student loans for international students?

What lenders refinance student loans for international students?

Lenders that refinance student loans for international students include SoFi, MPOWER, Earnest, and PNC among others. Generally, you’ll need to have a certain type of visa or be a permanent resident to be eligible. Check the specific eligibility requirements with each lender.

Do I need a U.S.-based cosigner to refinance my student loans?

A U.S.-based cosigner who is a citizen or permanent resident and has strong credit, a steady job, and a good income may strengthen an international student’s application for student loan refinance. That’s because lenders look at a borrower’s credit history and income when deciding whether to issue a loan. A cosigner takes equal responsibility for the loan and repays it in the event the primary borrower can’t.

What are the alternatives if I can’t refinance my student loans?

If you are unable to refinance your student loans, you could create a budget to save money and then put the money you save toward your loan payments to help pay down your debt faster. You can also pay more toward the principal on your loan each month, which may help you pay off your loans faster.

You can look into student loan consolidation if you have federal student loans and want to simplify the payment process, or income-based repayment plans if you’re trying to lower your federal monthly loan payment.

How does refinancing affect my credit score as an international student?

If you are able to refinance your loan as an international student, it could help build your credit over time as long as you consistently make your monthly payments by the due date. When you refinance and make on-time payments, you are helping to build a credit history for yourself, which could make it easier to be approved for loans or credit cards in the future.

Is refinancing worth it if I plan to return to my home country?

You will still be responsible for paying off your student loans if you return to your home country. So if refinancing gets you a lower rate or more favorable loan terms, it may be worth doing.

SoFi Student Loan Refinance SoFi Loan Products

Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

SOSLR-Q225-026