Guide to Exercising Stock Options

The employee stock option plans you may get through your employer can feel complicated, laden with technical terminology, and require strategic decision-making. It isn’t easy to know the best time to exercise stock options to reap the benefits of the plans. And it sure doesn’t help that the information sessions about stock purchase plans provided by work are usually dry and overwhelmingly unhelpful.

But being able to buy the shares of your company’s stock can be an ideal way to make and invest money. Thus, it is crucial to understand how stock options work, including knowing when to exercise stock options.

What Does It Mean to Exercise Employee Stock Options?

Employee stock options (ESOs) are rights to purchase an employer’s stock at a set price – called the exercise, grant, or strike price – for a set period of time. You exercise the option to buy the company’s stock at the strike price.

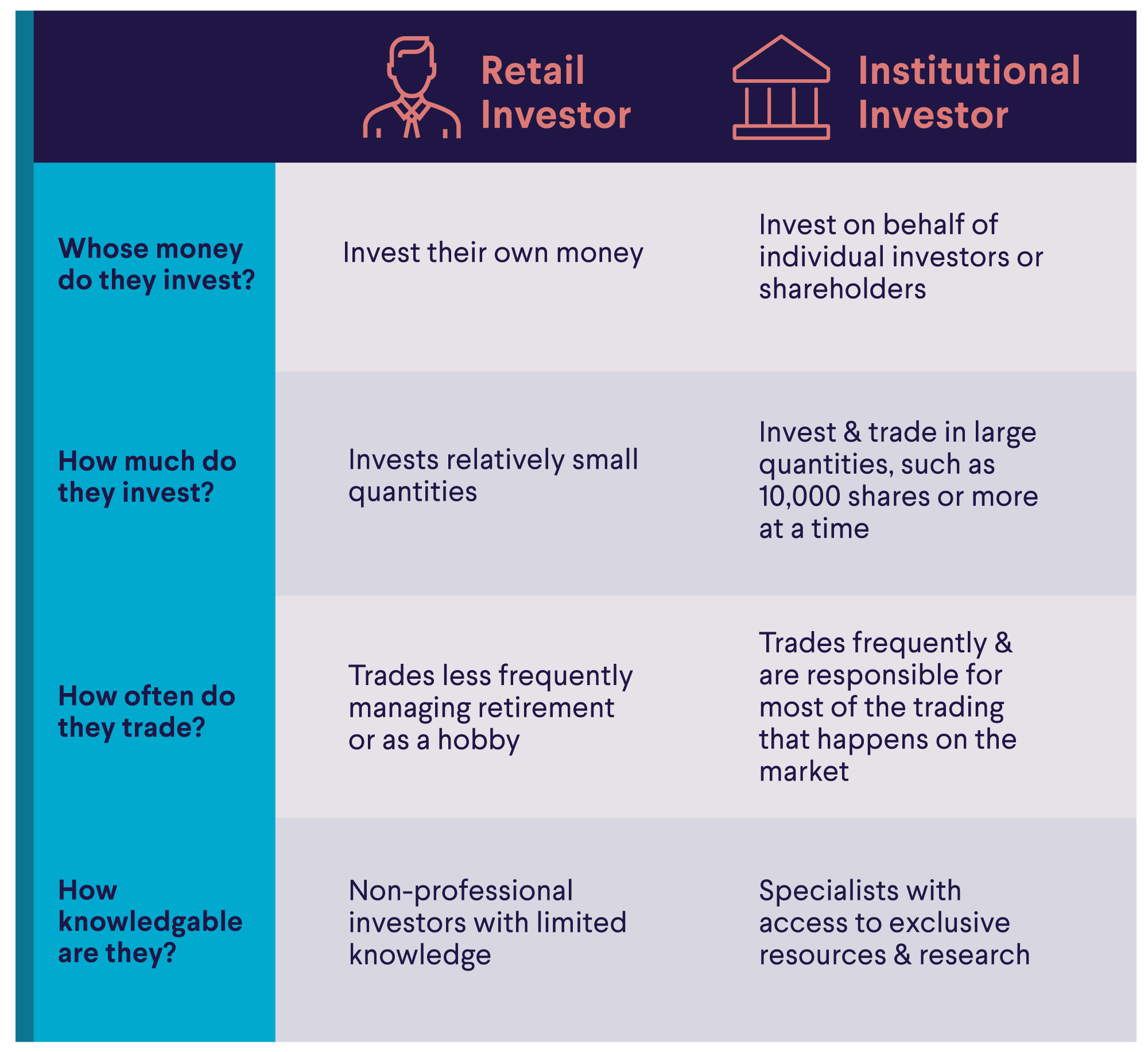

Employee stock options are similar to but different from exchange-traded stock options.

Companies may offer stock options to employees as part of a compensation plan, in addition to salary, 401(k) matching, and other benefits. In an ideal scenario, stock options allow an employee to purchase shares of their company’s stock at an exercise price lower than the current market price.

Employees should keep in mind that employee stock options are different from restricted share units (RSUs), another form of compensation.

💡 Recommended: How Are Employee Stock Options and RSUs Different?

Example of Exercising Stock Options

To exercise stock options, you must first be “vested,” meaning you have worked at the company for a specific period. As you vest, you can exercise your stock options.

For example, say you have 100 fully vested stock options after a three-year waiting period. These stock options have an exercise price of $10 and have a current market value of $20.

If you were to exercise your options right now, you would buy 100 shares of stock at $10 per share, or 50% off the stock’s current price. You could then turn around and sell the stock at $20 per share, earning $1,000 in the transaction. This discount is called the “bargain element.”

100 shares x $10 exercise price = $1,000 purchase price

100 shares x $20 market price = $2,000 market price

$2,000 – $1,000 = $1,000 profit

However, you don’t have to sell the stock when you exercise stock options; you may hold the stock as part of your investment portfolio.

Types of Employee Stock Options

Stock option plans come in two flavors: qualified and non-qualified, which refer to their taxation. Incentive stock options (ISOs) are qualified and have a more favorable tax treatment than non-qualified stock options (NSOs), which do not have as favorable taxation.

When you exercise ISOs and hold the shares for a certain period, you will be taxed at the more favorable capital gains tax rate when you sell the shares. You aren’t taxed when you exercise ISOs.

In contrast, NSOs are taxed as regular income when you exercise them and then taxed at the capital gains rate when you sell the shares.

You’ll want to consider these tax implications before you exercise your stock options.

Get up to $1,000 in stock when you fund a new Active Invest account.*

Access stock trading, options, auto investing, IRAs, and more. Get started in just a few minutes.

When To Exercise Stock Options

The first step to exercising stock options is determining whether you can exercise them. Under most stock option programs, employees can exercise the options after a designated vesting period outlined in an equity compensation agreement. These programs operate similarly to a 401(k) match program; the idea is to reward only employees who have been at the company for a certain amount of time.

Additionally, stock options usually come with an expiration date, which is the final date you can exercise the option. The expiration date is usually between 7 and 10 year from the date of the option grant, though it can be shorter if you leave the company. Many people wait until the last moment to exercise their options, but you may want to exercise stock options earlier. This means that you actively decide to exercise your options before the expiration date.

So, employees can exercise stock options after they vest and before an expiration date, a period known as the exercise window.

How to Exercise Stock Options

You can use three main strategies to exercise your vested stock options. Usually, your company will work with a third party to manage stock options, and you can initiate these transactions in your account.

Exercise and Hold

If you like the prospects of your company’s stock and want to add it to your investment portfolio, you can initiate an exercise-and-hold order. With this strategy, you purchase the shares at the exercise price with cash and hold on to them. You may need to deposit cash into your account or borrow on margin to pay for your shares. Additionally, you have to pay brokerage commissions, fees, and taxes.

An exercise-and-hold strategy allows you to benefit from the ownership of your employer’s stock, including any dividends and capital appreciation.

Exercise and Sell to Cover

Similar to exercise-and-hold, you may initiate an exercise-and-sell-to-cover order if you like the prospects of your company’s stock and want it as part of your portfolio. With an exercise-and-sell-to-cover order, however, you don’t necessarily need cash to buy the shares at the exercise price. Instead, an exercise-and-sell-to-cover order will sell enough shares to cover the purchase price, commissions, fees, and taxes.

An exercise-and-sell-to-cover order allows you to benefit from the ownership of your employer’s stock without using your cash to cover the transaction.

Exercise and Sell

If you are interested in making a cash profit rather than holding on to your employer’s stock, you can initiate an exercise-and-sell order. When you exercise with this transaction, you buy the company’s stock at the exercise price and sell the shares at the market price simultaneously. A portion of the proceeds cover the commissions, investment fees, and taxes, but you get to keep the rest of the cash profit.

Knowing Whether to Exercise Stock Options

Let’s say your stock options are vested, and any other required waiting periods are satisfied. Now, you have to decide whether to exercise your stock options now or wait until a later time.

From a stock valuation standpoint, deciding to exercise stock options is difficult. It is hard to know whether a company’s stock will go up or down in the near future — even the company you work for.

Here are a few reasons why people choose to exercise their stock options.

Options Have Lots of Value

When your stock options are in the money, meaning that your company’s stock price is above your stock option exercise price, you may be interested in exercising the option. In this situation, you can benefit from buying shares at a lower price to either make a profit or hold on to the stock.

Fits Your Financial Situation

Many people may choose to exercise their stock options and then sell the shares as a way to diversify their portfolios. You never want to be overly exposed to one stock, especially the stock of the company you work for. So, people will exercise their stock options, sell the shares, and use the proceeds to buy other securities as part of greater portfolio diversification.

Why Do People Not Exercise Stock Options?

Many people may not exercise stock options for a variety of reasons. One of the biggest reasons is that the stock options may be out of the money, meaning that the company’s stock price is below the stock option exercise price. If you exercised your stock options in this situation, you’d be buying the shares at a premium; you’d be better off buying the shares at the market price.

And even if your stock options are in the money, you may not exercise immediately, hoping your employer’s stock price will increase further.

Here are a few other reasons people may not exercise their stock options.

Fees

As mentioned above, you must account for commissions, fees, and taxes when exercising your stock options. And depending on an individual’s financial situation, they may not be able to pay the cash to cover those costs. Therefore they will hold off from exercising their stock options until they may be able to cover the expenses.

Expiration Date

Employee stock options often have an expiration date. Usually, the expiration date is between seven and ten years, but it may be shorter if you leave a company. Many employees do not know when they are nearing the expiration date of their stock options, so they may forget to exercise their options, potentially leaving money on the table.

Begin Investing with SoFi

While employee stock options may seem like a great piece of a compensation plan, you should also consider the risks. Generally, experts recommend that investors don’t keep more than 10% of their wealth in any one stock. This is especially true for the company that you work at. If something happens to the company that puts you out of a job, it could be potentially devastating to have a large piece of your net worth tied up in that company.

Suppose you have a large piece of your investment portfolio tied up in company stock after you exercised your stock options. In that case, it is a good idea to have your eye on eventually moving at least some of this money into a diversified investment strategy. Fortunately, a SoFi Invest® online brokerage account can help. With SoFi, you can build a diversified portfolio by trading stocks, exchange-traded funds, and fractional shares with no commissions for as little as $5.

Choose how you want to invest.

Ready to

do-it-yourself?

Want to take a

hands-off role?

FAQ

Can you exercise an employee stock option?

If you have an employee stock option plan through your employer, you can exercise your stock options as long as you’re vested and the options have not expired.

How soon should you exercise a stock option?

Knowing when to exercise a stock option is up to the individual, as everyone has different financial needs and goals. However, you want to ensure you exercise your stock options before expiration.

What are exercised stock options?

Exercised stock options are options that have been used to purchase shares of stock.

SoFi Invest® INVESTMENTS ARE NOT FDIC INSURED • ARE NOT BANK GUARANTEED • MAY LOSE VALUE

1) Automated Investing and advisory services are provided by SoFi Wealth LLC, an SEC-registered investment adviser (“SoFi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC.

2) Active Investing and brokerage services are provided by SoFi Securities LLC, Member FINRA (www.finra.org)/SIPC(www.sipc.org). Clearing and custody of all securities are provided by APEX Clearing Corporation.

For additional disclosures related to the SoFi Invest platforms described above please visit SoFi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform.

Options involve risks, including substantial risk of loss and the possibility an investor may lose the entire amount invested in a short period of time. Before an investor begins trading options they should familiarize themselves with the Characteristics and Risks of Standardized Options . Tax considerations with options transactions are unique, investors should consult with their tax advisor to understand the impact to their taxes.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

SOIN0622030