What Is the Mortgage Principal and How Does Paying It Down Work?

Many homebuyers swimming in the pool of new mortgage terminology may wonder how mortgage principal differs from their mortgage payment. Simply put, your mortgage principal is the amount of money you borrowed from your mortgage lender.

Knowing what your mortgage principal is and how you can pay it off more quickly than the average homeowner could save you a lot of money over the life of the loan. Here’s what you need to know about paying off the principal on a mortgage.

Key Points

• Mortgage principal is the original amount borrowed to pay for a home, distinct from the monthly mortgage payment or the home’s purchase price.

• Every month you make a payment on your mortgage, and principal, interest, and escrow accounts for taxes and insurance are typically all paid from that amount.

• Making extra payments toward principal can help pay off the mortgage early and reduce interest costs over the life of the loan.

• Amortization schedules show how each mortgage payment is split between principal and interest, with earlier payments mostly going toward interest.

• Benefits of paying additional principal on a mortgage are building equity, lowering interest costs, and shortening the loan term, but it should be considered in the context of overall financial priorities.

Mortgage Principal Definition

Mortgage principal is the original amount that you borrowed to pay for your home. It is not the amount you paid for your home; nor is it the amount of your monthly mortgage payment.

Each month when you make a payment on your mortgage loan, a portion goes toward the original amount you borrowed, a portion goes toward the interest payment, and some goes into your escrow account, if you have one, to pay for taxes and insurance.

Your mortgage principal balance will change over the life of your loan as you pay it down with your monthly mortgage payment, as well as any extra payments. This changing balance may be called your outstanding mortgage principal. (While there is a difference between outstanding mortgage principal vs. mortgage principal balance, the terms are often used interchangeably.) Your equity will increase while you’re paying down the principal on your mortgage.

Mortgage Principal vs Mortgage Interest

Your mortgage payment consists of both mortgage principal and interest. Mortgage principal is the amount you borrowed. Mortgage interest is the lending charge you pay for borrowing the mortgage principal. Both are included in your monthly mortgage payment, and your mortgage statement will likely include a breakdown of how much of your monthly mortgage payment goes to mortgage principal vs. interest.

When you start paying down principal, as the mortgage amortization schedule will show you, most of your payment at this point will go toward interest rather than principal. Later on in the life of your loan, you’ll be paying more mortgage principal vs. interest.

Hover your cursor over the amortization chart of this mortgage calculator to get an idea of how a given loan might be amortized over time if no extra payments were made.

Mortgage Principal vs Total Monthly Payment

Your total monthly payment is divided into parts by your mortgage servicer and sent to the correct entities. It includes principal plus interest, and often other components.

Fees and Expenses Included in the Monthly Payment

Your monthly payment isn’t typically just made up of principal and interest. Most borrowers are also paying installments toward property taxes and homeowners insurance each month, and some pay mortgage insurance, too. In the industry, this is often referred to as PITI, for principal, interest, taxes, and insurance.

A mortgage statement will break all of this down and show any late fees.

Escrow for Taxes and Insurance

Among the many mortgage questions you might have for a lender, one should be whether you’ll need an escrow account for taxes and insurance or whether you can pay those expenses in lump sums on your own when they’re due. Many lenders prefer to take on the responsibility for your taxes and insurance in order to protect their investment, but they will charge you for those costs in your mortgage payments and hold that money in an escrow account until needed.

Conventional mortgages typically require an escrow account if you borrow more than 80% of the property’s value. In the world of government home loans, FHA and USDA loans need an escrow account, and lenders usually want one for VA-backed loans. If you live in a flood zone and are required to have flood insurance, an escrow account may be mandatory.

Private Mortgage Insurance (PMI)

When you get a conventional loan and put down less than 20% of the home’s value, your lender will require you to pay private mortgage insurance (PMI).It will probably want to handle this through an escrow account also, to avoid the possibility of your making late payments.

Benefits of Paying Additional Principal on Mortgage

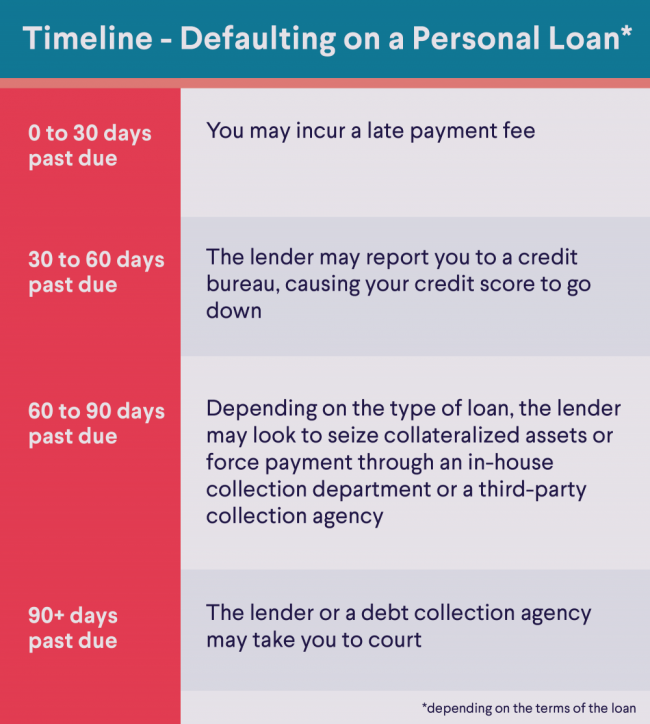

Making extra payments toward principal will allow you to pay off your mortgage early and will decrease your interest costs, sometimes by an astounding amount.

If you make extra payments, you may want to let your mortgage servicer know that you want the funds to be applied to principal instead of the next month’s payment.

Could you face a prepayment penalty? Conforming mortgages signed on or after January 10, 2014, cannot carry one. Nor can FHA, USDA, or VA loans. If you’re not sure whether your mortgage has a prepayment penalty, check your loan documents or call your lender or mortgage servicer.

Reducing Interest Over Time

If you make additional payments toward your principal, you will decrease the amount of money that you’re being charged interest on, as your principal balance drops. This means that in the long run, you would end up paying less interest than if you simply made your payments as scheduled.

Shortening the Loan Term

It can be helpful – and motivating – to keep an eye on how your mortgage payments are impacting your principal balance and how much of them is going to interest. There are a couple of easy ways to do this.

Amortization Schedules

An amortization schedule can be a big help in understanding your mortgage payments and how you’re paying down principal on your mortgage. Essentially, it’s a chart that lists each planned payment for the entirety of your mortgage, detailing how much of each will go to principal and how much to interest. You’ll also see how much principal you still owe after each payment.

To get a full amortization schedule for the life of your loan, you may need to sign on to your account online or contact your lender and request the schedule.

Mortgage Statements

The easiest way to keep track of how much you’re currently paying on your mortgage principal and interest is to look at your mortgage statements every month. The mortgage servicer will send you a statement with the amount you owe and how much it will reduce your principal each month. You may also see the breakdown for your previous payment and/or for the year to date, as well as your total outstanding mortgage principal. If you have an online account, you can usually see the numbers there.

How to Pay Down Mortgage Principal Balance

Paying off the mortgage principal is done by making extra payments. Because the amortization schedule is set by the lender, a high percentage of your monthly payment goes toward interest in the early years of your loan.

When you make extra payments or increase the amount you pay each month (even by just a little bit), you’ll start to pay down the principal instead of paying the lender interest.

It pays to thoroughly understand the different types of mortgages that are out there.

Biweekly Payment Strategy

One tactic homeowners use is biweekly payments. Traditionally, you pay your mortgage once a month. But if you pay it every two weeks – which often aligns with pay schedules – you’ll be making an extra payment every year. That may not sound like much, but it can let you finish your loan term up to six or more years early.

Applying Windfalls Toward Principal

A relatively painless way to prepay principal is to apply any “extra” money you get – like a work bonus or an unexpected bequest – toward your principal. If you have a solid emergency fund in place and no higher-interest debts to pay off, this could be a good place to put your money.

The Takeaway

Knowing exactly how mortgage principal, interest, and amortization schedules work can be a powerful tool that can help you pay off your mortgage principal faster and save you a lot of money on interest in the process.

Looking for an affordable option for a home mortgage loan? SoFi can help: We offer low down payments (as little as 3% - 5%*) with our competitive and flexible home mortgage loans. Plus, applying is extra convenient: It's online, with access to one-on-one help.

FAQ

What is the mortgage principal amount?

The mortgage principal is the amount you borrow from a mortgage lender and must pay back. It is not the same as your mortgage payment. Your mortgage payment will include both principal and interest, as well as any escrow payments you need to make.

How do you pay off your mortgage principal?

You can pay off your mortgage principal early by paying more than your mortgage payment. Since your mortgage payment is made up of principal and interest, any extra that you pay can be taken directly off the principal – just make sure that your lender knows you want the extra funds applied there. If you never make extra payments, you’ll take the full loan term to pay off your mortgage.

Is it advisable to pay extra principal on a mortgage?

Paying extra on the principal will allow you to build equity, pay off the mortgage faster, and lower your costs on interest. Whether you can fit it in your budget or if you believe there is a better use for your money depends on your personal situation.

What is the difference between mortgage principal and interest?

Mortgage principal is the amount you borrow from a lender; interest is the amount the lender charges you for borrowing the principal.

Can the mortgage principal be reduced?

When you make extra payments or pay a lump sum to your lender, you can specify that those funds should be applied to your mortgage principal. This will reduce your principal and your interest payments.

Does your monthly principal payment change?

Yes. Since loans are typically amortized, at the beginning of the loan term, most of your monthly payment will be applied toward your interest charges. Over time, that balance will shift as you pay down your mortgage, and principal will be most of each payment that you make closer to the end of your loan. Your decreasing principal amount is sometimes called your outstanding mortgage principal vs. mortgage principal balance.

Photo credit: iStock/PeopleImages

*SoFi requires Private Mortgage Insurance (PMI) for conforming home loans with a loan-to-value (LTV) ratio greater than 80%. As little as 3% down payments are for qualifying first-time homebuyers only. 5% minimum applies to other borrowers. Other loan types may require different fees or insurance (e.g., VA funding fee, FHA Mortgage Insurance Premiums, etc.). Loan requirements may vary depending on your down payment amount, and minimum down payment varies by loan type.

SoFi Mortgages

Terms, conditions, and state restrictions apply. Not all products are available in all states. See SoFi.com/eligibility-criteria for more information.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

¹FHA loans are subject to unique terms and conditions established by FHA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. FHA loans require an Upfront Mortgage Insurance Premium (UFMIP), which may be financed or paid at closing, in addition to monthly Mortgage Insurance Premiums (MIP). Maximum loan amounts vary by county. The minimum FHA mortgage down payment is 3.5% for those who qualify financially for a primary purchase. SoFi is not affiliated with any government agency.

†Veterans, Service members, and members of the National Guard or Reserve may be eligible for a loan guaranteed by the U.S. Department of Veterans Affairs. VA loans are subject to unique terms and conditions established by VA and SoFi. Ask your SoFi loan officer for details about eligibility, documentation, and other requirements. VA loans typically require a one-time funding fee except as may be exempted by VA guidelines. The fee may be financed or paid at closing. The amount of the fee depends on the type of loan, the total amount of the loan, and, depending on loan type, prior use of VA eligibility and down payment amount. The VA funding fee is typically non-refundable. SoFi is not affiliated with any government agency.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

SOHL-Q325-035

Read more