What Happens When Your Student Loans Go to Collections?

When a borrower stops making payments on student loans for a period of time, they could end up in default. And in some cases, lenders may send defaulted loans onto collections.

If your student loans end up in collections, it can have serious financial consequences. Your credit score may be damaged, and sometimes your wages may be garnished. While it can be very stressful, there are steps you can take to fix the problem.

Table of Contents

- How Student Loans End Up in Collections

- What Does It Mean to Have a Loan Sent to Collections?

- What Happens When Your Loans Go into Default and Collections?

- How to Get Your Loans Out of Default

- What to Do If Your Student Loan Goes to Collections

- Preventing Default: Refinance Student Loans

- The Takeaway

- FAQ

Key Points

• When student loans go into collections, it can severely impact credit scores and may lead to wage garnishment.

• Collections agencies are tasked with recovering debts and may charge additional fees.

• Engaging with collections agencies can lead to possible repayment negotiations or plans.

• Federal student loans allow wage garnishment without a court order, unlike private loans which require legal action.

• Defaulting on student loans can result in losing eligibility for further federal aid and damage financial standing.

How Student Loans End Up in Collections

Student loans don’t go away until you’ve paid them off. If you haven’t been paying off your student loans, your debt can go into default because you are failing to fulfill your contractual obligation to repay your loan.

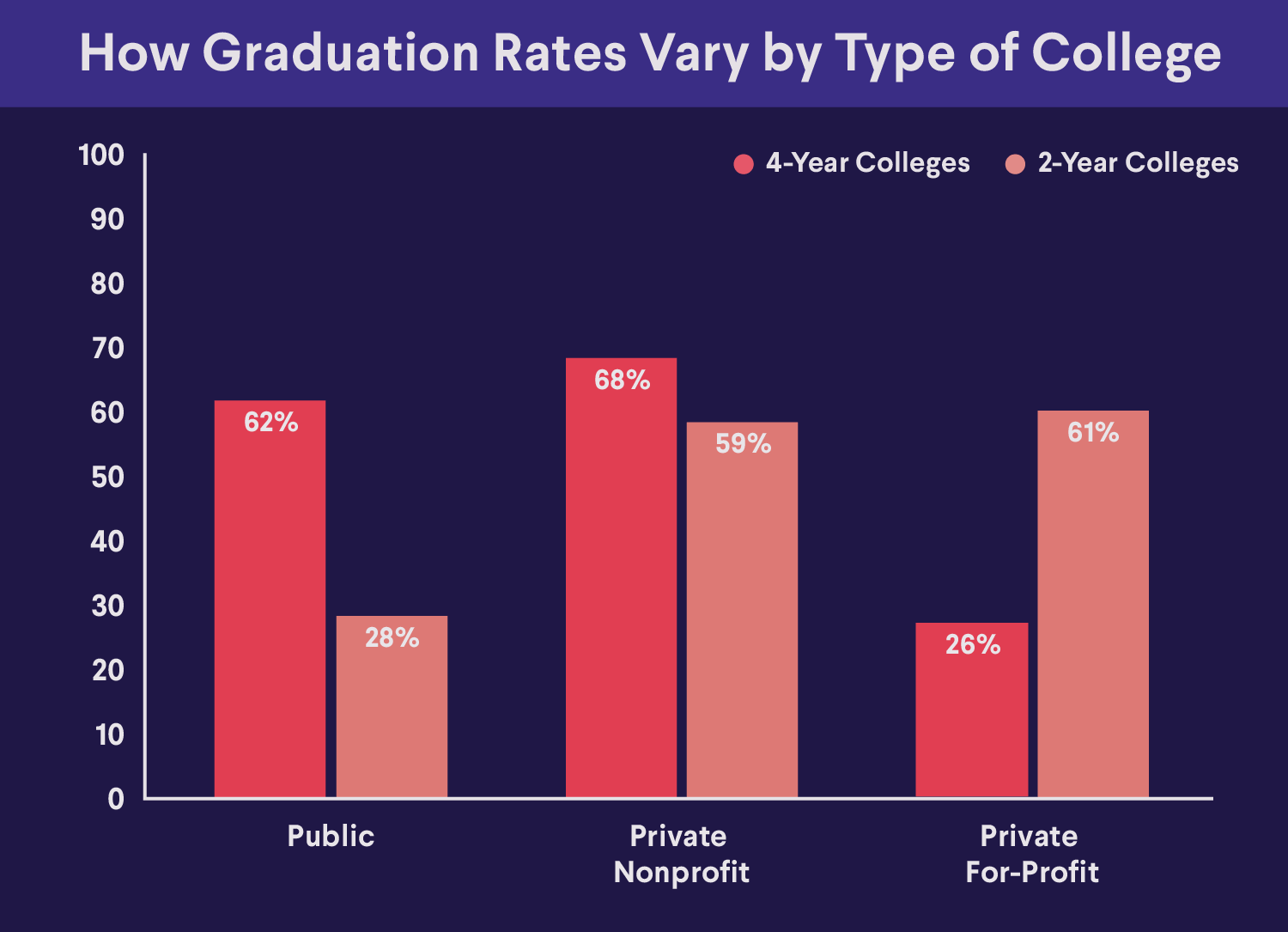

Americans owe $1.77 trillion in student loan debt as of 2025. When you consider that the average federal student loan debt is more than $37,000 per borrower, it’s no surprise that some have trouble keeping up with it. In fact, an average of 6.24% of student loans are in default at any given time.

Delinquent Federal Student Loans

The first day after missing a payment on a federal student loan, the loan becomes delinquent. The loan will remain delinquent until the overdue balance is paid or the borrower makes alternate arrangements, such as applying for deferment or forbearance or switching their payment plan.

After 90 days of missing payments for federal student loans, the loan servicer will report the late payments to credit bureaus, which could negatively impact the borrower’s credit score.

Federal Student Loans in Default

For federal student loans, you typically go into default after you haven’t paid your loan bill for nine months or 270 days. When in default, the entire balance of the loan comes due. But just because a loan is in default, doesn’t mean it automatically goes to a collections agency.

At this point, you may have the opportunity to make arrangements with your loan servicer. For example, your lender may help you tailor solutions that lower your monthly bill to make payments more manageable for you.

However, if you don’t come to an agreement, your lender can send your debt to a collections agency that will collect it for them.

Recommended: Defaulting on Student Loans: What You Should Know

Private Student Loans in Default

The timeframe may vary for private loans depending on the terms and conditions of the loan. Generally speaking, private student loans may go into default after 90 days of missed payments. You should read your loan agreement for more information on when your loan provider will send your defaulted loans to collections.

Refi now to pay off loans &

reach your goals faster with a shorter term.

What Does It Mean to Have a Loan Sent to Collections?

Once your debt is sent to a collections agency, that agency will do everything they can to get you to pay. Unfortunately, on top of collecting the debt, collections agencies typically charge fees.

Once your debt is in collections, the collections agency might try to work out a repayment plan with you as a first step. If you continue to not pay, the agency can then take actions to recoup the money, such as trying to garnish your wages.

Garnishment means the agency can take a certain amount from each paycheck and apply it toward your debt — in the case of federal student loans, it cannot be more than 15%. For federal student loans, lenders are not required to take the borrower to court before garnishing wages.

Private student loans function differently. They are not subject to the same special regulation as federal student loans. Private lenders interested in garnishing wages must follow garnishment rules laid out for private debt. In this case, the lender is required to take the borrower to court and obtain a judgment in their favor before any wages can be garnished.

Recommended: What Happens If You Just Stop Paying Your Student Loans

What Happens When Your Loans Go into Default and Collections?

Some other not-so-great things can happen when your loans go into default and collections.

First, if you have defaulted on federal student loans, you may lose access to various federal loan repayment plans and forbearance or deferment on federal loans. These programs are important tools designed to make it easier for you to pay off your loans. Loan forgiveness is offered to those who have jobs in certain government, healthcare, and nonprofit sectors. Forbearance allows you to temporarily stop making student loan payments or reduce the amount you pay each month.

Your credit score may take a hit, as well. With both private and federal student loans, the lender or the collections agency will report the late payments to the three major credit bureaus, and that might then lower your credit score.

A low credit score might cost you down the line, making it difficult to secure future loans at reasonable interest rates. It may even mean you won’t qualify for a loan at all.

How to Get Your Loans Out of Default

The best thing you can do to avoid your student loans going into default and being sent collections is to pay your bills on time. If you think you’re going to miss a payment, reach out to your loan provider to see if they’ll offer support.

But if you’ve defaulted, there may still be options for you to recover.

Options for Federal Student Loans

If you have federal student loans, you can try to rehabilitate your student loan in collections. Here’s how the program works: After you’ve made three consecutive on-time, voluntary, full payments on a defaulted federal loan, you can consolidate your federal loans.

The new direct loan pays off the old loans in full and consolidates them. Once you have made nine out of 10 consecutive, voluntary, on-time payments to this new loan, the loan may be rehabilitated and the default may be removed from your record.

With a Direct Consolidation Loan, your eligible federal loans will be combined into one loan with a fixed interest rate — and the new rate will be the weighted average of the rates on the loans being consolidated (rounded up to the nearest one-eighth of 1%).

Options for Private Student Loans

When it comes to private student loans, private lenders may or may not offer borrowers the opportunity to rehabilitate their loans. You should contact your lender and ask what you can do to get your loan out of default. Sometimes borrowers who have rehabilitated a private student loan may ask to have the default removed from their credit report, but there is no guarantee that it will be removed.

Additionally, it’s important to note that some lenders may charge off private student loans that are delinquent for 120 days, or a set period of time, which may vary from lender to lender. When a lender charges off a loan, it means they have written off the loan as a loss and close the account. They typically sell your loan to a debt buyer or collections agency, but you are still legally obligated to pay off the loan. If the debt is charged off, the lender may not be willing to work with the borrower.

What to Do If Your Student Loan Goes to Collections

If you do find yourself in the unfortunate situation of having debt in collections, there might be steps you can take.

First, you could talk to your collections agency. Remember: Collections agencies want you to pay. It’s in their best interest for you to ultimately pay back your loan. In many ways, this is a situation in which the ball is in your court.

When you talk to them, the collections agency might offer payment options tailored to your individual circumstances, depending on if you’re employed and how much money you earn.

They might offer solutions such as allowing you to pay a discounted lump sum, or they might set up a manageable monthly payment plan if you don’t have much income.

Having your loans in default or collections might have serious effects on your credit and your financial stability. If you’re afraid of defaulting on your loans, or if you already have, consider taking action as fast as you can. Taking control of the situation could help keep it from getting worse.

Preventing Default: Refinance Student Loans

Refinancing student loans can be a strategic move to prevent default by lowering monthly payments and interest rates. When you refinance, you replace your existing loans with a new one that often has more favorable terms, making it easier to manage your debt. This can provide much-needed relief, especially if you’re struggling with high interest or a tight budget.

Keep in mind, though, that when you refinance federal student loans with a private lender, you lose access to federal benefits, such as student loan forgiveness and income-driven repayment plans.

The Takeaway

In an ideal world, the best way to avoid going into student loan default is to make payments on time and in full. If you have competing financial priorities, however, it may be difficult for you to pay your loans on time.

If your student loans end up in collections, it may damage your credit score, and with federal loans, your wages may be garnished. There are steps you can take to rehabilitate your defaulted loans, depending on whether you have private or federal loans.

To avoid default, it’s best to make your payments on time. If you’re struggling to make your payments, consider student loan refinancing.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

FAQ

What happens when student loans are sent to collections?

When student loans are sent to collections, your credit score drops, and you face increased interest rates and fees. Collection agencies may contact you frequently, and you could experience wage garnishment, tax refund offsets, and legal action.

What happens if you never pay off student loans?

If you never pay off student loans, consequences include damaged credit, wage garnishment, tax refund offsets, and potential legal action. Federal loans can also lead to loss of eligibility for federal benefits and increased interest. Private loans may result in more aggressive collection tactics.

How long can student loans stay in collections?

Student loans can remain in collections indefinitely, but the impact on your credit score typically diminishes over time. However, collectors can continue to pursue repayment, and the debt may be sold to other collection agencies, leading to ongoing financial and legal issues.

SoFi Student Loan Refinance SoFi Loan Products

Terms and conditions apply. SoFi Refinance Student Loans are private loans. When you refinance federal loans with a SoFi loan, YOU FORFEIT YOUR ELIGIBILITY FOR ALL FEDERAL LOAN BENEFITS, including all flexible federal repayment and forgiveness options that are or may become available to federal student loan borrowers including, but not limited to: Public Service Loan Forgiveness (PSLF), Income-Based Repayment, Income-Contingent Repayment, extended repayment plans, PAYE or SAVE. Lowest rates reserved for the most creditworthy borrowers. Learn more at SoFi.com/eligibility. SoFi Refinance Student Loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

SOSLR-Q325-012

Read more